Market Frenzy: Fed’s Fateful Rate Decision & Big Tech Earnings Collide This Week

Brace for impact—this week’s economic fireworks could send shockwaves through every portfolio. The Fed’s rate decision looms like a sword of Damocles, while Big Tech’s earnings reports threaten to either turbocharge or tank the markets.

Will Powell blink? Wall Street’s betting on dovish whispers, but crypto traders know better—central banks love to ‘surprise’ when liquidity’s already thin.

Meanwhile in Techland: The Magnificent Seven face their reckoning. AI hype meets revenue reality, and shareholders are sweating bullets. One mediocre guidance away from another ‘efficiency restructuring’ (read: mass layoffs dressed as innovation).

Pro tip: When the VIX spikes, Bitcoin’s your best hedge—unless you still think fiat printers go brrr forever.

TLDR

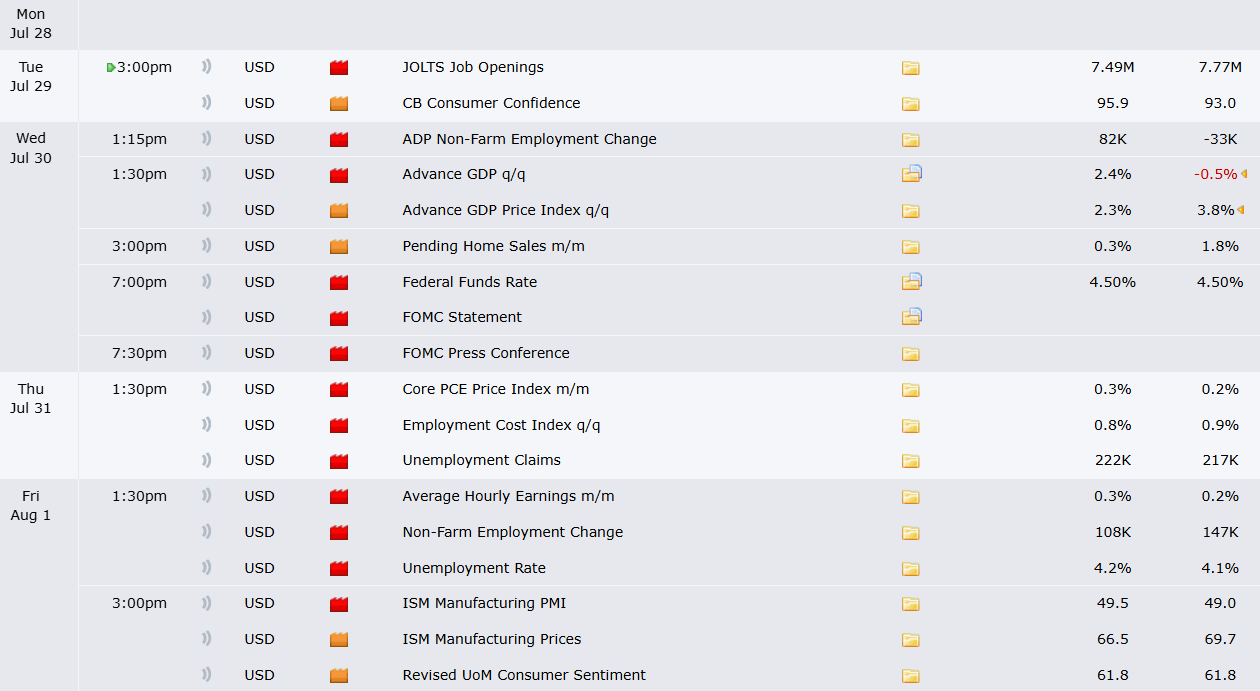

- Federal Reserve meeting scheduled this week with no rate cut expected, markets pricing only 3% chance

- July jobs report expected to show 101,000 new jobs added with unemployment rising to 4.2%

- Big Tech earnings from Apple, Amazon, Microsoft, and Meta will focus on AI spending plans

- Second quarter GDP expected to show 3% growth after first quarter contraction

- 164 S&P 500 companies reporting earnings this week with current growth at 6.4%

Stock markets closed at record levels as investors prepare for an intense week of economic data and corporate earnings. The S&P 500 gained 1.5% last week with five consecutive record closes.

The Federal Reserve will announce its policy decision Wednesday with no rate changes expected. Markets show only a 3% probability of a cut this month according to CME FedWatch data.

Fed Governor Christopher Waller suggested he might support lowering rates at this meeting. However, most analysts expect the central bank to wait until September for any policy changes.

September rate cut odds stand at 64% for at least a quarter-point reduction. JPMorgan’s Michael Feroli predicts attention will focus on potential dissenting votes among committee members.

Economic data releases include second quarter GDP figures on Wednesday. Forecasts call for 3% annualized growth following the first quarter’s 0.5% decline.

Employment Data Takes Priority

The July jobs report arrives Friday with expectations for 101,000 new payrolls. Unemployment is projected to rise slightly to 4.2% from June’s 4.1% rate.

June employment data showed 106,000 jobs added while joblessness unexpectedly dropped. Economic conditions suggest steady labor market trends continuing through year-end.

Thursday’s Core PCE inflation reading should show 0.3% monthly growth in June. This represents an acceleration from May’s 0.2% increase while annual inflation holds at 2.7%.

Corporate earnings season continues with 164 S&P 500 companies reporting results. Current earnings growth runs at 6.4% based on companies already reported.

Technology Sector in Spotlight

Apple, Amazon, Microsoft and Meta will deliver quarterly results this week. Artificial intelligence spending plans remain the primary investor concern following Alphabet’s increased capital expenditure guidance.

Google’s parent company raised 2025 spending projections by $10 billion to $85 billion total. Other technology firms face questions about their AI investment strategies and returns.

Additional major companies reporting include Boeing, Coinbase, Exxon Mobil, Chevron and Starbucks. The earnings season shows companies beating estimates while maintaining forward guidance.

This differs from recent quarters where companies reduced future projections after strong results. Citi’s Scott Chronert calls this “beat-and-hold” pattern supportive of continued market gains.

Analyst projections for late 2025 and 2026 earnings continue rising. Current estimates show 13.9% growth expected for 2026, up from 13.8% forecasts one month ago.

Goldman Sachs tracking of speculative trading activity shows elevated levels. Their indicator measuring unprofitable stocks and richly valued companies approaches dot-com bubble and 2021 SPAC levels.

Historical patterns suggest strong near-term market performance but weaker medium-term results following such speculative surges. Trade negotiations also continue with Friday marking another presidential deadline for deal completion.