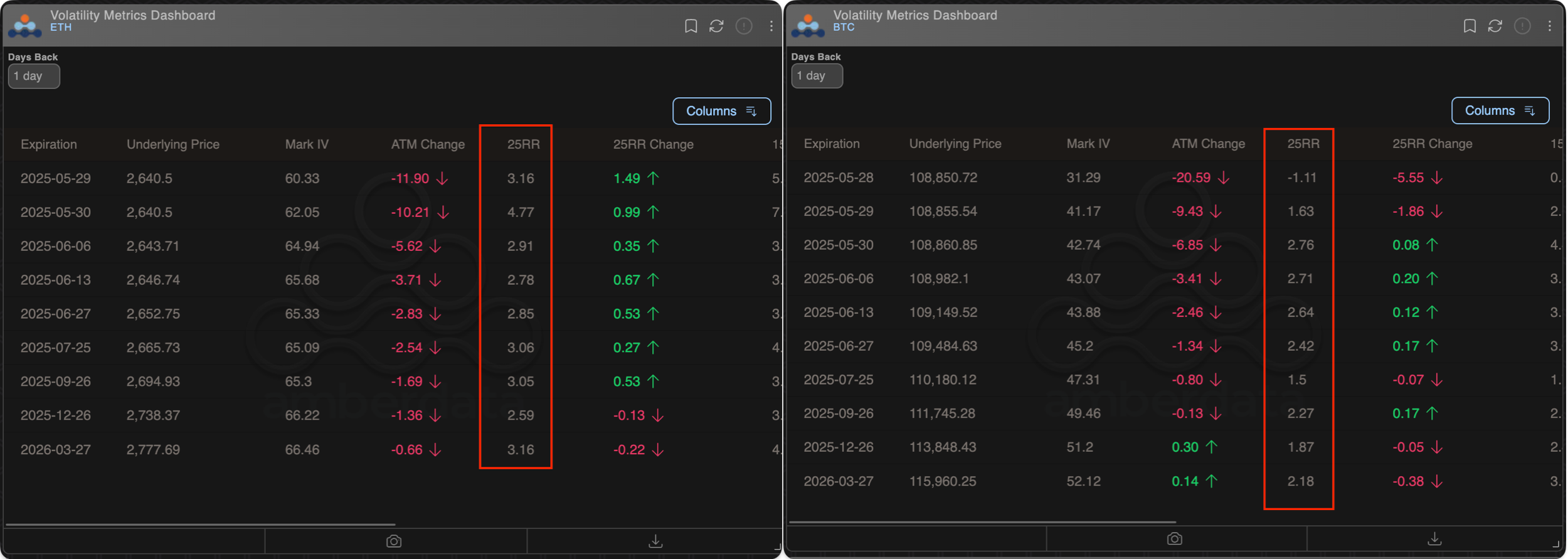

Whales Are Dumping Bitcoin for Ethereum—Here’s Why

Big money’s flipping the script—Ethereum’s stealing Bitcoin’s lunch, and the charts don’t lie. Three smoking guns point to a seismic ETH power grab.

First up: Institutional inflows. ETH products just saw their third straight week of positive flows while BTC funds bled out. Wall Street’s voting with its wallet—and surprise, they’re not actually nostalgic for 2017 memes.

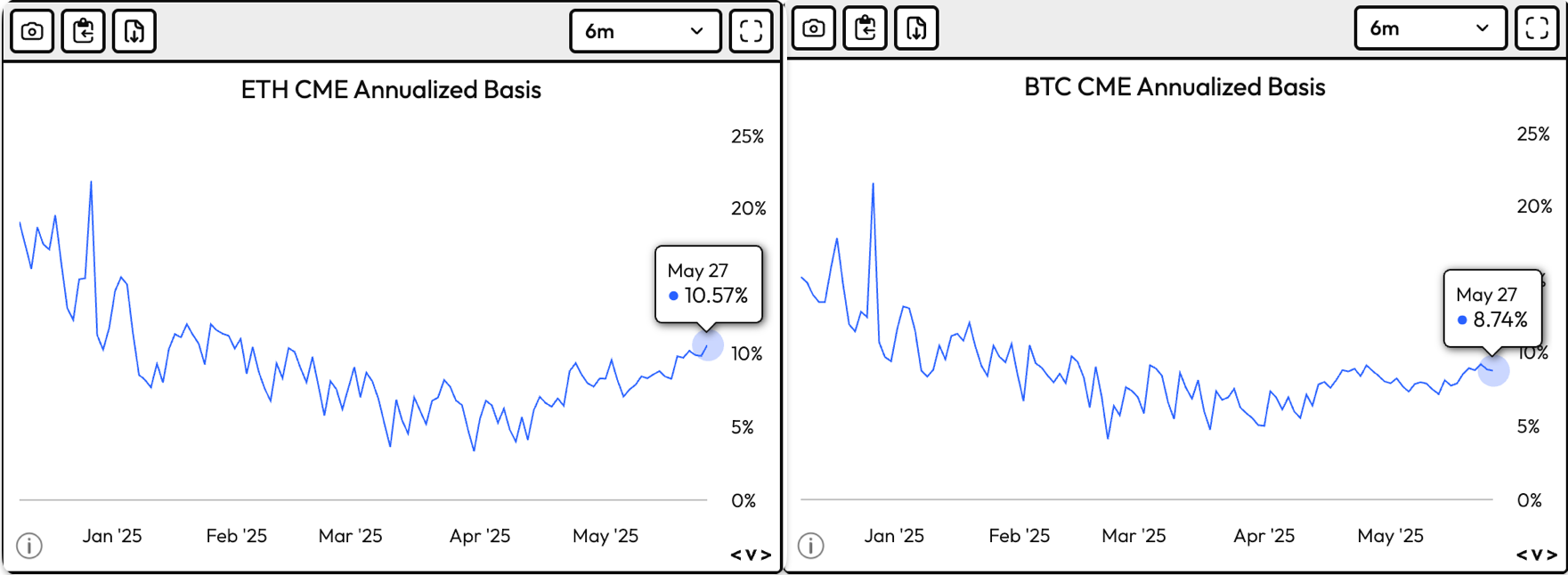

Then there’s the futures curve. ETH contango widened to 8% annualized this week—double Bitcoin’s premium. Traders are paying up for leverage, a classic bull market tell.

Finally, the options market’s gone full YOLO. ETH’s 25-delta skew flipped positive as demand for calls exploded. Meanwhile, Bitcoin’s volatility got dumped like a bag-holder’s Telegram promises.

So is this the ‘flippening’? Maybe not yet—but when the suits start treating ETH like the new reserve asset, even the most delusional Bitcoin maxi should check their pulse. (Or their portfolio.)

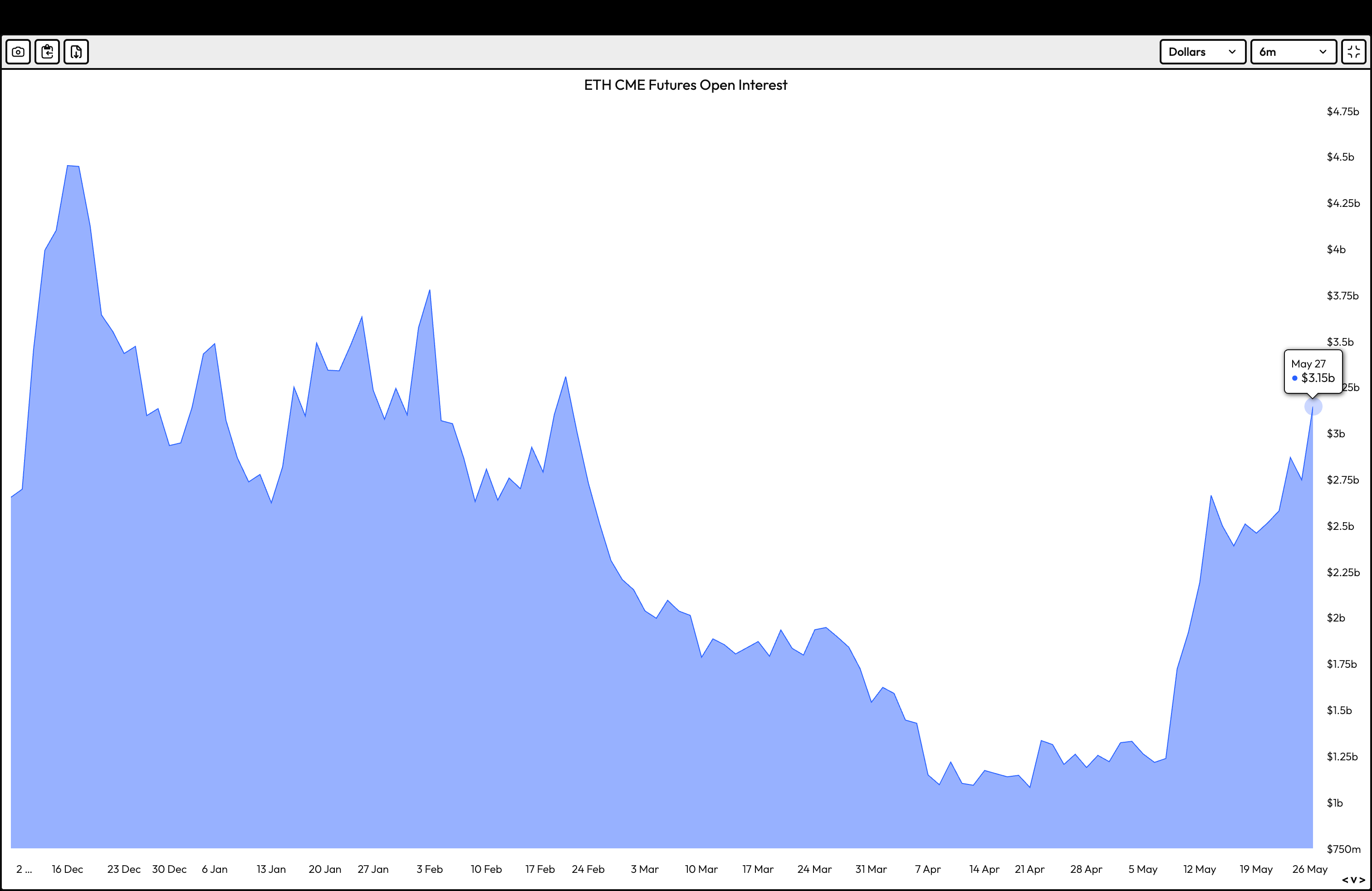

CME futures open interest

CME futures open interest

The notional open interest in CME bitcoin futures, which represents the dollar value of the number of active contracts, has risen by roughly 70% to over $17 billion since the early April crash, according to data source Velo.

The growth, however, has stalled above $17 billion over the past seven days. The CME is considered a proxy for institutional activity.

Meanwhile, ether’s open interest has jumped 186% to $3.15 billion since the early April crash. The growth has accelerated over the past two weeks.

The diverging trends show institutions are increasingly leaning toward ether.

The bias for ETH is also evident from the relative richness of premiums in ether futures.

As of the time of writing, one-month Ether futures boasted an annualized premium of 10.5%, the highest since January, according to Velo. Meanwhile, Bitcoin futures premium was 8.74%.

Elevated premiums indicate Optimism and strong buying interest, often signaling a bullish trend. Therefore, the relative richness of ether futures premium suggests traders are more bullish on ETH compared to BTC. After all, ether is still 84% short of record highs reached during the 2021 bull run.

There is also a possibility that the BTC’s basis may have been held lower by cash and carry arbitrage (non-directional) traders.

A similar divergence is observed on offshore exchanges, where annualized funding rates, representing the cost of holding long positions in ETH perpetual futures, has neared the 8% mark. Meanwhile, BTC’s funding rates hold below 5%.