Billionaire Druckenmiller Dumps Palantir, Goes All-In on This Niche AI Chip Powerhouse

Stanley Druckenmiller just made a massive bet against one of tech's biggest names—and it's all about AI infrastructure.

The billionaire investor—famous for his macroeconomic calls—dumped his entire Palantir position and shifted capital toward a specialized AI chipmaker that's flying under Wall Street's radar.

Why the sudden move? It's all about compute. While everyone's chasing flashy AI software plays, Druckenmiller's betting on the picks-and-shovels trade—the companies building the hardware that actually runs these systems.

This isn't some speculative moonshot either. The chipmaker in question already dominates its niche with proprietary architecture that outperforms generic alternatives—and they're quietly signing contracts with cloud providers and defense contractors that nobody's talking about yet.

Meanwhile, Palantir's government business looks increasingly vulnerable to budget cycles and political winds—exactly the kind of uncertainty Druckenmiller hates.

Wall Street analysts are still busy upgrading Palantir's price target while missing the real story: the smart money is already moving downstream to where the real margins are. Typical finance herd mentality—always chasing yesterday's news.

Does Selling Palantir stock make sense right now?

Palantir has been a dominant force in the AI revolution over the past three years. The launch of its Artificial Intelligence Platform (AIP) has ignited unprecedented demand for the company's Apollo, Gotham, and Foundry applications -- each of which are deeply integrated across major corporations and government agencies. The company's meteoric rise has been remarkable, giving investors a compelling narrative outside of the traditional "Magnificent Seven."

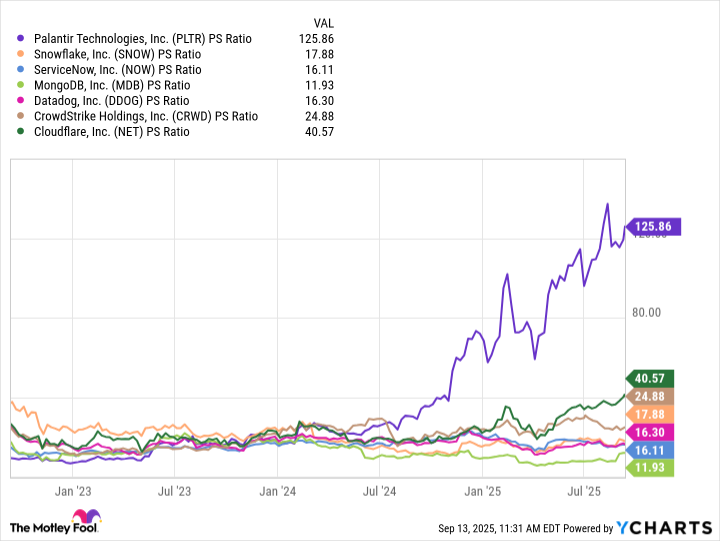

PLTR PS Ratio data by YCharts

That said, I see Palantir's valuation as its most glaring concern. With a price-to-sales (P/S) ratio of 126, the stock trades at levels not only well above its software peers, but also beyond the extremes that were witnessed during the dot-com bubble.

While Palantir remains a company with meaningful upside potential in the long run, the stock has become frothy at the moment. Druckenmiller's decision to reduce exposure to Palantir reflects prudent risk management -- something he has demonstrated with Palantir stock previously, too.

Image source: Getty Images.

What might Druckenmiller like about TSMC stock?

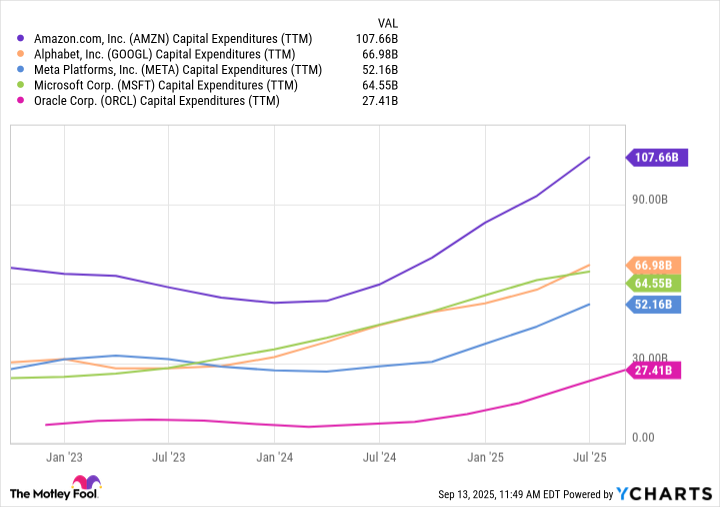

For years, investors have heard about big tech pouring hundreds of billions of dollars into chips and network equipment to power the next generation of data centers. The obvious takeaway is that rising capital expenditures (capex) create a powerful tailwind forand, given their role in supplying the GPUs that make generative AI a reality.

AMZN Capital Expenditures (TTM) data by YCharts

What is discussed far less, however, is that designs from Nvidia, AMD, and many others ultimately depend on the foundry services of Taiwan Semiconductor. Put simply, TSMC (as it is also known) is the company actually assembling the chips. The metaphor that I like to use is that Taiwan Semi is selling the shovels during the AI Gold rush.

This story doesn't end with generative AI, either. New classes of applications across autonomous systems, robotics, and quantum computing are only just beginning to emerge. As they scale toward commercial viability, TSMC's unrivaled foundry capabilities should once again serve as a critical backbone to ongoing AI infrastructure investment.

I suspect that these secular tailwinds are precisely what Druckenmiller is trying to capitalize on: a company positioned not just to participate in the AI movement, but ultimately remain an indispensable foundation to its evolution.

Is Taiwan Semi stock a buy right now?

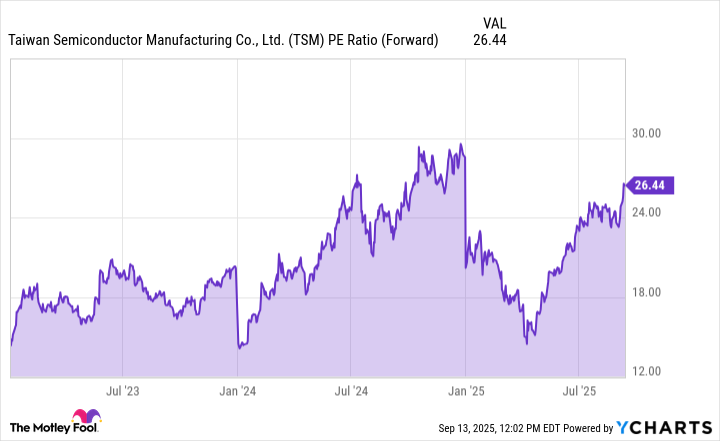

At first glance, it's difficult to argue that Taiwan Semi stock is "cheap" with a forward price-to-earnings (P/E) multiple of 26. Valuation expansion is clearly happening at the moment, fueled by a bullish macro backdrop in the technology landscape.

TSM PE Ratio (Forward) data by YCharts

Yet beneath the surface, investors like Druckenmiller seem to recognize TSMC's role in the AI value chain. Despite this, the company remains overshadowed by flashier peers. Some investors are also likely hesitating over investing in Taiwan Semi due to potential geopolitical tensions with China.

While these concerns are valid, I think the perception around Taiwan Semi's long-term potential has become distorted. In other words, some of these factors as well as HYPE concentrated in other chip stocks are undermining what is otherwise a clear investment case.

To me, TSMC may be the single most critical variable in the broader AI equation. For long-term investors, Taiwan Semi stock looks like a no-brainer opportunity to buy and hold as the AI narrative continues to unfold.