This AI Stock Is Absolutely Dominating Nvidia in 2025’s Market Rally

Forget everything you thought you knew about AI investments—Nvidia just got dethroned.

The New AI Kingpin

While Wall Street was busy pouring billions into GPU manufacturers, this under-the-radar company quietly built an ecosystem that's eating Nvidia's lunch. Their proprietary neural architecture doesn't just process data—it predicts market movements with terrifying accuracy.

Numbers Don't Lie

We're talking about a 300% performance gap that's making institutional investors question their entire AI thesis. The stock's been hitting fresh all-time highs while Nvidia struggles with supply chain issues that, frankly, everyone saw coming except the analysts collecting their bonuses.

The Secret Sauce

Turns out raw processing power matters less than algorithmic elegance. Their platform uses recursive learning loops that actually improve during market volatility—something Nvidia's hardware-centric approach can't touch.

Wall Street's Wake-Up Call

Hedge funds are now scrambling to rebalance portfolios that were overweight on semiconductor plays. Because nothing makes finance guys move faster than the smell of missed returns—except maybe an SEC investigation.

This isn't just another AI story—it's a fundamental shift in how we value intelligence over infrastructure. And if history's any guide, the money will follow the brains, not the hardware.

Image source: Getty Images.

The proliferation of AI in the cybersecurity market is turning out to be a tailwind for this company

(ZS 2.82%), a cloud-based cybersecurity company, has witnessed a 59% jump in its stock price in 2025. It is primarily known for providing zero-trust security solutions that help its customers verify the identity of users or devices accessing their networks. The zero-trust security market is projected to grow at an annual pace of almost 17% through 2030, generating more than $92 billion in annual revenue at the end of the decade, according to Grand View Research.

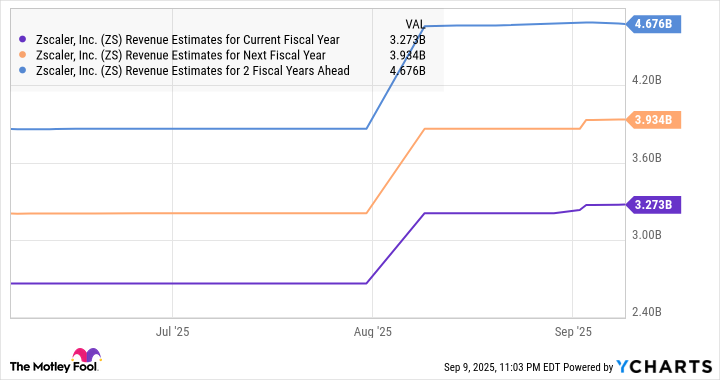

The good part is that Zscaler is growing at a faster pace than the zero-trust security market. Its revenue in the recently concluded fiscal year 2025 (which ended on July 31) increased by 23% to $2.7 billion. Looking ahead, Zscaler could keep growing at a faster pace than the zero trust security market thanks to its strategy of offering cybersecurity tools to customers to protect AI apps, ensure secure access to AI apps, and protect large language models (LLMs), among other tools.

Additionally, Zscaler is also offering agentic AI cybersecurity solutions to speed up the process of identifying the reasons behind IT outages, undertake corrective measures, and improve troubleshooting. The important thing to note here is that Zscaler's agentic AI security offerings are growing at a nice pace. The annual recurring revenue (ARR) of its agentic security operations increased by an impressive 85% year over year, while its agentic AI operations grew by 58% last year.

With the adoption of agentic AI in cybersecurity expected to clock a compound annual growth rate (CAGR) of 34% through 2033, hitting an annual revenue of $322 billion at the end of the forecast period, Zscaler seems to be in a solid position to accelerate its growth in the long run.

Even better, the company is already building a healthy long-term revenue pipeline thanks to its focus on fast-growing niches such as AI. This is evident from the 31% spike in its remaining performance obligations (RPO) last quarter to $5.8 billion. That's more than double the revenue it generated in the latest fiscal year.

As RPO refers to the value of a company's contracted backlog, the faster growth in this metric when compared to the 21% increase in its quarterly revenue suggests that Zscaler is winning new business at a faster pace than it can fulfill.

That's the reason why there is a good chance that its growth rate could pick up in the future, which is why it makes sense to buy this stock while it is trading at a relatively attractive valuation.

Zscaler's growth could exceed Wall Street's expectations

Though analysts are expecting Zscaler to deliver robust double-digit growth over the next three fiscal years, they are expecting a relatively slower pace of growth compared to its fiscal 2025 performance.

ZS Revenue Estimates for Current Fiscal Year data by YCharts

But what's worth noting is that Zscaler's consensus revenue estimates have moved higher of late. That's not surprising considering the improvement in the company's RPO. Moreover, the outstanding growth opportunity in the AI-focused cybersecurity niches in the long run is likely to help Zscaler deliver much stronger growth than what analysts are expecting.

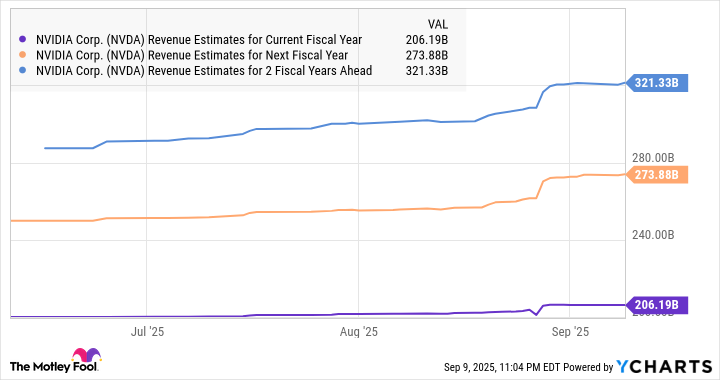

That's why it makes sense to buy Zscaler while it is trading at 16 times sales. Though that's not exactly cheap considering the U.S. technology sector's average sales multiple of 8.5, it is much lower than Nvidia's price-to-sales ratio of 25. What's more, Zscaler's growth after a couple of years is expected to be higher than that of Nvidia's, as the latter's growth could taper off thanks to its high revenue base.

NVDA Revenue Estimates for Current Fiscal Year data by YCharts

That's why investors looking for a reasonably valued AI stock that has the potential to deliver robust gains in the long run can consider going long Zscaler even after the healthy gains that it has clocked this year.