3 Reasons I’m Buying Nvidia’s Stock Like There’s No Tomorrow

Nvidia's chips are eating the world—and I'm loading up before Wall Street catches up.

AI Dominance Isn't Slowing Down

Every major tech player needs their hardware. From data centers to autonomous vehicles—Nvidia's GPUs remain the undisputed king of AI processing. Demand isn't cooling; it's accelerating.

Supply Chain Control = Pricing Power

While competitors scramble for manufacturing capacity, Nvidia locks in partnerships and secures supply. That means they set the rules—and the prices. Margins stay fat while others fight for scraps.

The Ecosystem Play

It's not just hardware. CUDA, software suites, developer networks—Nvidia built a moat so wide that switching costs became prohibitive. They don't just sell chips; they sell the entire infrastructure.

Sure, valuation looks stretched—but since when did traditional metrics matter in tech? This isn't a stock; it's a ticket to the future. Buy before the herd realizes the old rules no longer apply.

Nvidia headquarters. Image source: Getty Images.

1. Data center capital expenditures are still rising

Nvidia's primary products, graphics processing units (GPUs), have been in huge demand thanks to the AI race. They have become the computing unit of choice for training and running these models, and that dominance doesn't look to be faltering.

GPUs can process multiple calculations in parallel, leading to impressive performance. And they can be connected in clusters within a data center to create unparalleled computing power for AI applications.

Luckily for investors, Nvidia's largest clients are starting to offer guidance for 2026 capital expenditures (capex). A high percentage of this revenue will be used for data centers, with a hefty chunk going toward filing them with Nvidia GPUs. Even though 2025 was a record-setting year for capex, 2026 is expected to exceed these levels.

The company also expects this to continue rising through at least 2028. During its 2025 GTC event, management cited a third-party projection that estimated global data center capex at $400 billion during 2024. That's expected to rise to $1 trillion by 2028, which will be a huge growth boost for Nvidia.

This primary growth engine for the company is far from done, which bodes well for its future.

2. Nvidia's China business will return shortly

In April, the TRUMP administration revoked Nvidia's export license for its H20 chips, which were specifically designed to meet prior export regulations. This created a significant hole in the company's business, but that hole could be plugged shortly.

It reapplied for its export license with assurances from the government that it will be approved. However, there's one concession that the company may need to make.

The government plans to charge Nvidia a 15% export tax on these GPUs, which will eat into its profit margins. Even so, these chip sales to China will be a huge boost to its business, even if they aren't as profitable as they once were.

In the second quarter, its projected revenue growth WOULD have been 77% instead of the guidance figure of 50% if H20 chip sales were allowed. This boost could be coming as soon as the third quarter, providing another crucial growth lever.

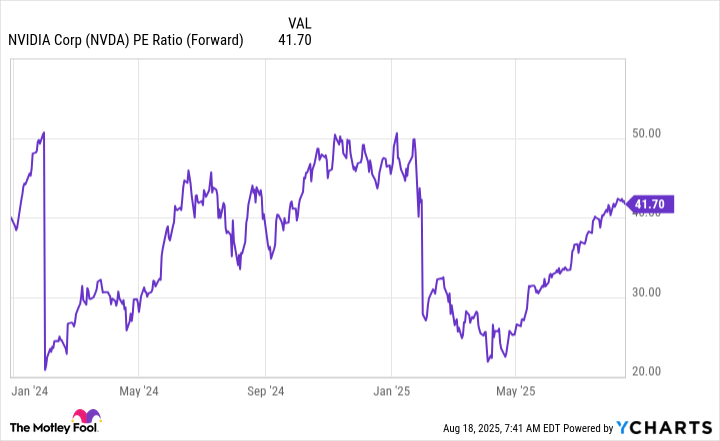

3. The stock isn't as expensive as it seems

Nvidia's rise hasn't been all business-related. Its stock has easily become the most popular in the market, which has caused its valuation to skyrocket. At 42 times forward earnings, it is far from cheap.

NVDA PE Ratio (Forward) data by YCharts; PE = price to earnings.

However, the company's growth is more than enough to offset that. If Wall Street analysts' projections for $5.91 in earnings per share (EPS) in fiscal 2027 (ending January 2027) turn out to be right, that indicates the stock trades for 31 times 2027 earnings, which is a far more reasonable price tag.

However, the average analyst only expects 27% revenue growth in fiscal 2027. If Nvidia outperforms projections (as it has often done), its profits could grow far quicker, leading to a cheaper stock price.

Its growth and size are hard to reconcile, which could make its future difficult to predict. But the company's China business is returning, and domestic AI demand is driving huge data center buildouts. These two factors could easily cause Nvidia to exceed expectations, making it a winning stock pick over the next few years.