Palantir Stock Just Skyrocketed Post-Earnings—Here’s the Shocking Truth About Whether to Sell Now

Palantir’s stock just ripped higher after earnings—but the real question isn’t whether it’s overbought. It’s whether Wall Street’s even asking the right questions.

### The AI Hype Train vs. Reality Check

Another quarter, another ‘AI-driven’ rally. Palantir’s bulls are pounding the table, while skeptics whisper about valuation voodoo. Who’s right? Follow the money—not the PowerPoint slides.

### The Institutional Game No One’s Talking About

Hedge funds aren’t buying Palantir for its gov contracts anymore. They’re front-running the retail FOMO. Again. Classic ‘pump-and-hold’—Wall Street’s favorite side hustle.

### To Sell or Not to Sell? (Spoiler: It’s Trickier Than You Think)

Trim on euphoria, buy on panic? Sure—if you enjoy gambling with algos that read Twitter faster than you blink. The real play? Watch the options flow. The big money’s already placing bets.

Bottom line: Palantir’s not a stock—it’s a volatility ETF disguised as a ‘tech disruptor.’ And until the Fed turns off the punch bowl, the party’s not over. Just don’t cry when they take away the balloons.

Image source: Getty Images.

An incredible business journey

The reason for Palantir's stock price appreciation is a miraculous comeback in its growth. In 2023, the company's revenue growth had slowed to around 12% year over year, even though it was barely generating $2 billion in revenue. Selling analytics and monitoring software is not a limitless addressable market, but Palantir clearly had a lot more potential if it could execute.

Then, the artificial intelligence (AI) revolution began. Palantir was perfectly preparing for the present moment with its AI-focused software, which has led to steady acceleration in revenue growth at greater scale. Last quarter, revenue grew 48% year over year and hit an annualized run rate of $4 billion, Profit margins have also shown steady progress, hitting 27% last quarter when the company was unprofitable just a few years ago.

A turnaround such as this is why Palantir shares are up 600% in the last year. It has reaccelerated revenue growth and looks to be building huge momentum with contract wins at businesses and the United States government. Last quarter alone, it closed 42 deals worth $10 million or more. This should lead to strong future revenue growth in the next few years.

Putting the valuation in context

After this recent run, Palantir now has a market cap of $425 billion. That makes it the 22nd most valuable company in the world by market capitalization. And yet, it has only hit a run rate of $4 billion in annual revenue.

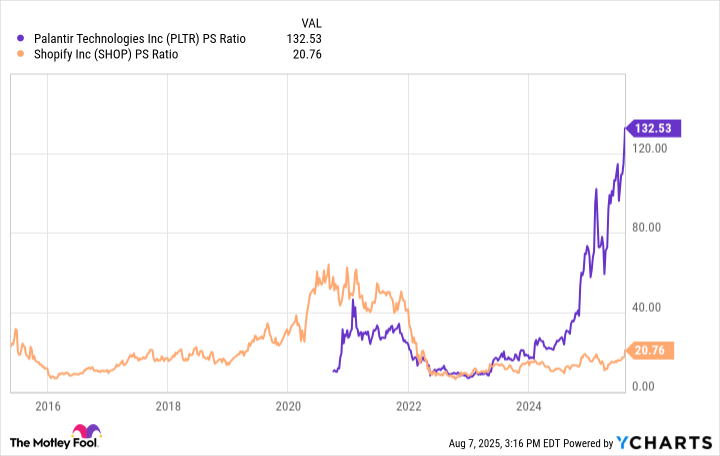

This puts Palantir's valuation at the extreme level, even for fast-growing software businesses. For context, one stock with a premium valuation in software is, and it has a price-to-sales ratio (P/S) of just over 20. Palantir's is 132. This gap -- where Palantir is valued at 5x or even more than a group of software stocks already with premium valuations -- should be front of mind for investors.

Even though Palantir has fantastic profit margins that may grow even more in the coming years, there is only so much margin expansion you can achieve. Profits cannot be higher than revenue, and Palantir is valued at an extreme level of revenue at the moment. The stock's only path forward to meet these high expectations are many years of strong double-digit revenue growth close to the levels it is at today.

PLTR PS Ratio data by YCharts

Should you sell Palantir stock?

I believe it is possible that Palantir can keep up its revenue growth of approximately 50% for the next few years. Its United States commercial revenue is growing at 93% year over year, which is propelling consolidated revenue to keep accelerating.

However, eventually you run out of enterprises and government agencies to sell software to. Software budgets are not infinite, and growth is bound to slow down once the AI boom tempers out. This should be a warning sign for Palantir shareholders, because the stock may need a bunch of years of huge revenue growth to warrant buying the stock at its current market cap.

Even if revenue grows by 10x over the next decade, the stock will still be trading at a premium price-to-sales ratio (P/S) of above 10, and that is assuming the stock price doesn't MOVE for a decade.

If you buy a stock, you want it to be likely that the share price will rise over a decade. Expectations are much too high on Palantir stock, and it is likely to greatly underperform the broad market indexes moving forward. It is time to sell, or at least trim, your Palantir position after this recent earnings pop.