Alameda Research Receives 500 BTC in Merchant Wallet - Crypto Giant’s Strategic Move Signals Market Confidence

Alameda Research just landed a massive 500 BTC deposit in its merchant wallet—fueling speculation about the trading firm's next big play.

Strategic Accumulation or Routine Operation?

That half-thousand Bitcoin injection represents serious capital movement in today's volatile market. While Alameda maintains its usual poker face about specific strategies, this kind of wallet activity typically precedes major market moves.

Market Impact and Industry Watching

Traders are closely monitoring the flow, knowing Alameda's track record for timing market entries with surgical precision. The 500 BTC transfer demonstrates continued institutional-level confidence in Bitcoin's fundamentals—even as traditional finance types still can't decide whether crypto is the future or just 'digital tulips.'

With this latest wallet activity, Alameda reinforces its position as a market maker that moves markets—proving once again that in crypto, real money talks while traditional finance still struggles to read the whitepaper.

Image source: Getty Images.

Reasons to buy Amazon

1. The stock's value

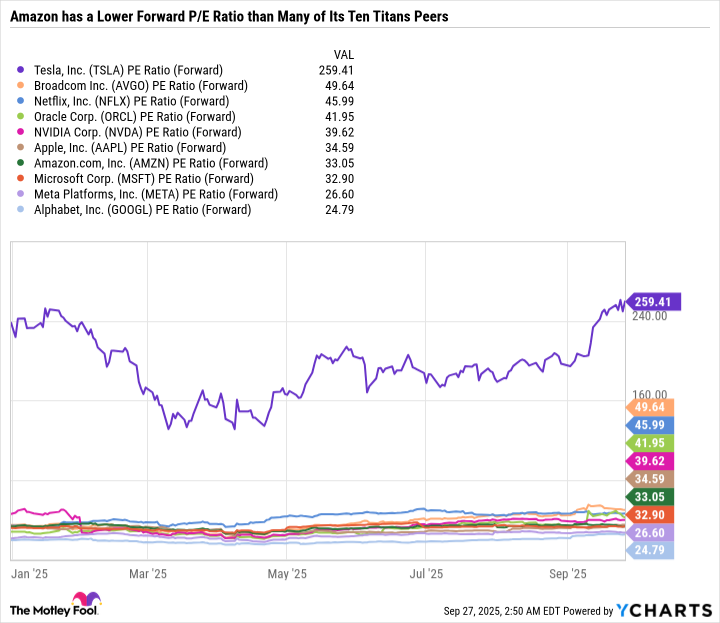

Amazon is a reasonable value, with the stock trading at 33.1 times forward earnings. That's less expensive than Apple, which isn't growing as quickly as Amazon.

TSLA PE Ratio (Forward) data by YCharts; PE = price to earnings.

Amazon invests in long-term projects, doesn't pay a dividend, and even dilutes its shareholders through stock-based compensation. Whereas many of its Ten Titans peers pay small dividends or at least repurchase enough stock to more than offset stock-based compensation, thereby avoiding share dilution.

Still, Amazon's attractive valuation is a reason to take a closer look at the stock.

2. AWS is the industry leader

Amazon is the undisputed leader in cloud computing. On its latest earnings call, for the second quarter, CEO Andy Jassy estimated that the second-largest cloud player (presumably Microsoft) is about 65% the size of Amazon Web Services (AWS). That's a commanding lead in an industry with decades of growth potential.

Being the market leader gives AWS a TON of exposure to different industries. It's also not solely dependent on artificial intelligence (AI) to drive cloud growth given its legacy position in general computing and basic enterprise services.

3. Amazon has other levers to pull outside of AWS

AWS is the crown jewel, but Amazon also owns Amazon Prime, Prime Video, MGM Studios, Amazon Music Prime, Prime Gaming, Twitch, Audible, Kindle, Whole Foods Market, Amazon Fresh, and healthcare services.

This diversification makes the company less dependent on any single market and provides numerous options for capital allocation. Amazon is one of those companies that is never short on ideas. Which is why it spends so aggressively.

Reasons to sell Amazon

1. Growth is slowing

Amazon's valuation has decreased for several valid reasons. The biggest being that growth has slowed.

In its most recent quarter, Amazon grew total sales by 13%, AWS revenue by 17.5%, and AWS operating income by 9.7%. These are decent results, but not great given Amazon's aggressive spending.

For the upcoming third quarter, Amazon is guiding for 10% to 13% revenue growth and operating income to be roughly flat year over year. The company's growth is under pressure due to a slowdown in AWS and strained consumer spending, which is affecting its e-commerce business.

2. AWS is losing ground to competitors

Arguably, the primary reason to pass on Amazon is the intense competition in cloud computing. Amazon has a commanding lead right now, but AWS' once seemingly impenetrable moat is showing cracks.

During its second-quarter earnings call, an analyst asked management why AWS was growing slower than the No. 2 and No. 3 cloud players. Jassy explained that AWS is well positioned from an AI standpoint and that customers care a lot about scale and security. He also said that it's still early for AWS and the industry, which is incredible considering AWS is a $123 billion run-rate business.

However, it's undeniable that both Microsoft Azure and Google Cloud are growing faster than AWS. And then there's Oracle, which is making the case for why there should really be the "big four" cloud giants rather than just the "big three."

Oracle is bringing over 70 data centers on line in just a few years. These are custom-built for AI and high-performance computing. They're fast, new, and ultra-efficient, which is why Oracle is landing huge contracts with OpenAI and Meta Platforms.

Oracle also partners with AWS, Azure, and Google Cloud by embedding native versions of its infrastructure into the big three clouds. This approach reduces latency by bringing AI to the dataset rather than moving huge datasets across cloud providers. With its pure-play business-to-business approach, Oracle is arguably the hottest AI growth stock to buy now.

Buying Amazon for the right reasons

At first glance, Amazon looks like a no-brainer buy given its reasonable valuation and noticeable underperformance compared to the rest of the Ten Titans. But dig deeper, and there are some flaws in the business that shouldn't go unnoticed.

Amazon is different than other companies. When Apple and Alphabet were getting clobbered earlier this year, it was easier to make the buy case because of their reasonable valuations, high free cash flow, and ability to return capital to shareholders. Amazon's aggressive spending leads to inconsistent free cash flow. In this vein, it deserves less slack than the other Ten Titans.

That said, investors who believe that consumer spending will improve and AWS' dominance is here to stay are getting the chance to buy Amazon at a good valuation in a market that is becoming increasingly expensive.