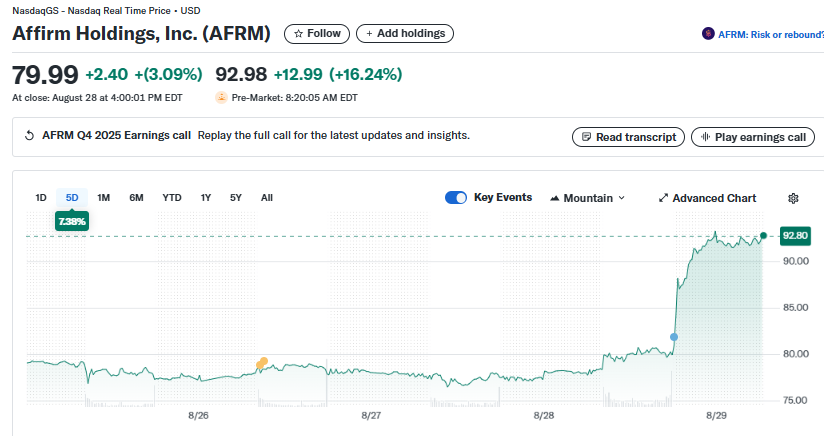

AFRM Stock Explodes 16%+ After Q4 Earnings Smash Expectations with 33% Revenue Surge

Affirm Holdings just delivered a knockout quarter that sent traders scrambling.

The Numbers Don't Lie

Revenue catapults 33% year-over-year—crushing analyst projections. The market responds instantly, driving shares up over 16% in after-hours trading. This isn't just a beat; it's a statement.

Why It Matters

Buy-now-pay-later isn't just surviving; it's thriving. While traditional credit card companies push predatory rates, Affirm's transparent model grabs market share. Consumers vote with their wallets—even if those wallets are digitally financed.

Wall Street's Love-Hate Dance

Another quarter, another dramatic swing. The same analysts who downgraded AFRM last month now scramble to upgrade targets. Classic finance whiplash—where conviction lasts exactly until the next earnings release.

TLDRs;

- Affirm shares soared 16.24% after reporting Q4 earnings of $0.20 per share, topping analyst expectations.

- Revenue surged 33% to $876 million, while GMV grew 43% to $10.4 billion.

- Net income hit $69.2 million, reversing a $45.1 million loss from the same period last year.

- Strong partnerships with Amazon, Shopify, and Apple helped offset the loss of Walmart, supporting growth momentum.

Affirm Holdings, Inc. (AFRM) saw its shares rally 16.24% on Friday, after the buy now, pay later (BNPL) company posted quarterly results that outpaced Wall Street expectations.

The fintech firm reported a revenue of $876 million, surpassing analyst estimates of $837 million, and delivered earnings of $0.20 per share, nearly double the LSEG consensus forecast of $0.11.

The upbeat report signals a strong rebound for Affirm, which has faced growing competition and regulatory challenges in recent years. Revenue climbed 33% year-over-year, while gross merchandise volume (GMV) or the total value of transactions processed, expanded 43% to $10.4 billion.

Profitability Returns After Last Year’s Loss

Perhaps the most notable figure in the report was Affirm’s return to profitability. The company posted net income of $69.2 million, a sharp turnaround from the $45.1 million loss recorded in the same quarter last year.

This profitability milestone demonstrates Affirm’s growing efficiency and resilience within the BNPL sector. Despite heavy competition from rivals such as Klarna, the firm has managed to balance scaling its operations with maintaining sustainable margins. Investors responded positively to the improvement, driving shares sharply higher in post-market trading.

Partner Diversification Strengthens Outlook

A key driver of Affirm’s growth has been its diverse roster of merchant partners. While the company lost a significant contract with Walmart earlier this year, when the retail giant shifted its BNPL offering to Klarna, Affirm’s partnerships with Amazon, Shopify, and Apple helped cushion the blow.

The strategy highlights the importance of partner diversification in the BNPL industry. Companies heavily reliant on one retailer risk sharp revenue swings if that partnership ends. By maintaining multiple high-profile alliances, Affirm has been able to sustain growth even amid competitive pressures.

Looking ahead, Affirm projects Q1 revenue between $855 million and $885 million and GMV between $10.1 billion and $10.4 billion. While slightly lower than Q4, these figures reflect steady momentum despite industry headwinds.

Affirm, $AFRM, Q4-25. Results:

📊 Adj. EPS: $0.69 🟢

💰 Revenue: $876M 🟢

📈 Net Income: $69M

🔎 Achieved profitability with $58M in operating income and record GMV of $10.4B, fueled by strong 0% APR loan adoption and Affirm Card growth. pic.twitter.com/bbeLh4EJay

— EarningsTime (@Earnings_Time) August 28, 2025

Regulatory Challenges Loom Over BNPL Sector

Affirm’s success comes at a time when the BNPL sector is under greater regulatory scrutiny. The Consumer Financial Protection Bureau (CFPB) has begun requiring BNPL providers to adopt rules similar to those governing credit card companies, citing concerns over consumer debt and repayment risks.

BNPL adoption has surged in the U.S., with loan volumes skyrocketing from $2 billion in 2019 to $24.2 billion in 2021, according to Federal Reserve data. Nearly two-thirds of U.S. consumers have been offered BNPL options, and around 14% used them within the last year.

For Affirm, the evolving regulatory environment presents both risks and opportunities. While compliance costs are expected to rise, established players like Affirm could benefit if tighter rules create barriers to entry for smaller competitors.