DeFi Lending Explodes Past $40B as Yield-Hungry Crypto Users Flood the Market

Yield chasers are pouring billions into decentralized lending protocols—tradFi banks are watching their margins evaporate in real time.

The $40B Milestone

DeFi isn't just competing with traditional finance anymore—it's eating its lunch. While banks offer fractional percentage points on savings accounts, decentralized platforms deliver double-digit APY without asking for permission. No branches, no paperwork, just pure yield extraction.

The Institutional Shift

Hedge funds and crypto whales are driving this surge, deploying capital across Compound, Aave, and emerging lending pools. They're not here for the ideology—they're here for the returns. Smart contracts don't care about your credit score, only your collateralization ratio.

The Risk Paradox

Higher yields come with smarter risks—impermanent loss, oracle failures, and contract vulnerabilities. But when traditional savings accounts lose to inflation, who's really taking the bigger gamble? DeFi offers transparency banks can only promise—every transaction on-chain, every rate algorithmically enforced.

Wall Street's worst nightmare? A system that proves financial intermediation doesn't require a skyscraper or a suit—just code that actually works.

DeFi lending has become one of the busiest spaces of the crypto market again. Instead of going after trades, more people are treating crypto like a savings account by parking stablecoins and tokens on platforms for steady yields.

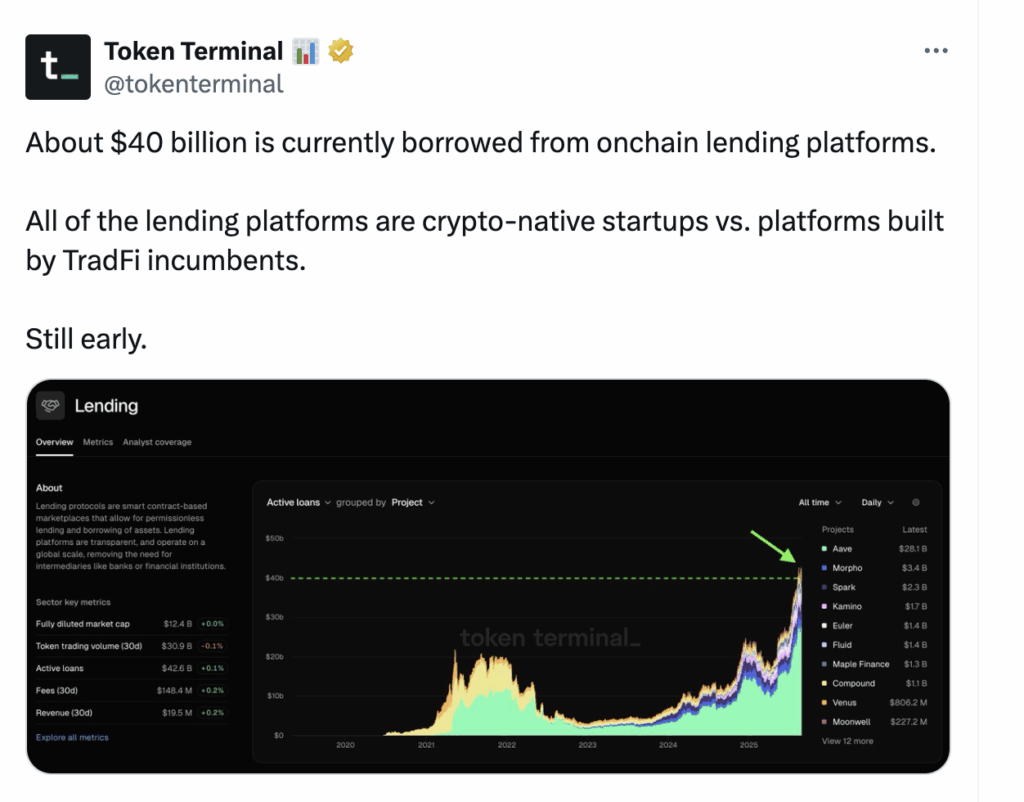

On the other side, traders borrow this liquidity to make Leveraged bets. This balance has now pushed active borrowing in DeFi past $40 billion (from a few protocols alone), the highest in over two years.

Stablecoins Are Driving DeFi Lending Growth

Stablecoins are at the heart of this shift. Depositors are supplying billions in USDT, USDC, and other stablecoins to lending markets, making up more than 70% of deposits.

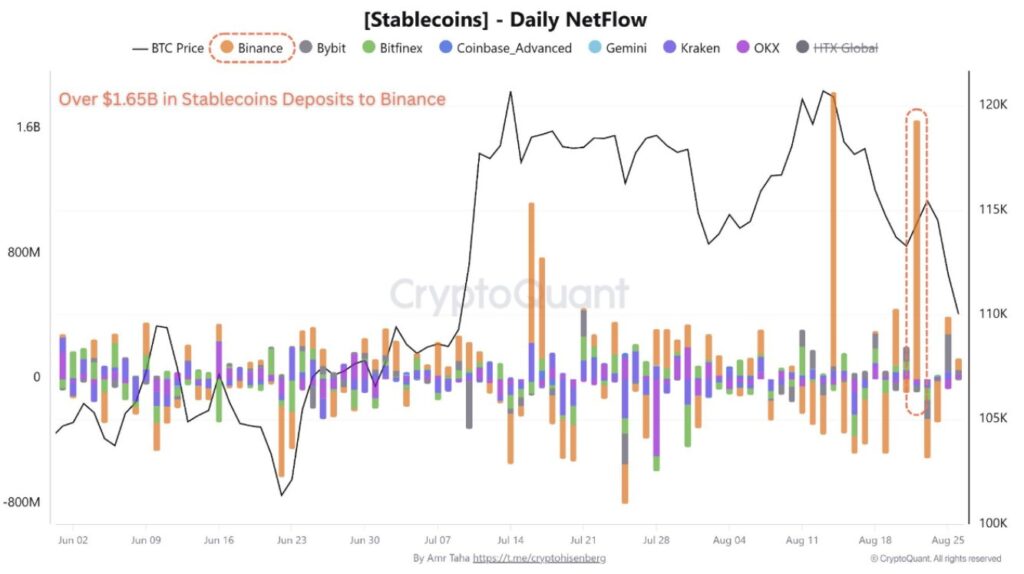

This matches the strong inflows reported on exchanges; Binance alone saw $1.65 billion in stablecoin deposits in a single day in late August.

Across the broader market, the stablecoin index has climbed nearly 10% in just six weeks, lifting the market cap close to $290 billion.

Solana even added $1 billion of stablecoin supply in a single week, reflecting how liquidity is moving across multiple chains.

On the borrowing side, active loans crossed $42.6 billion in late August.

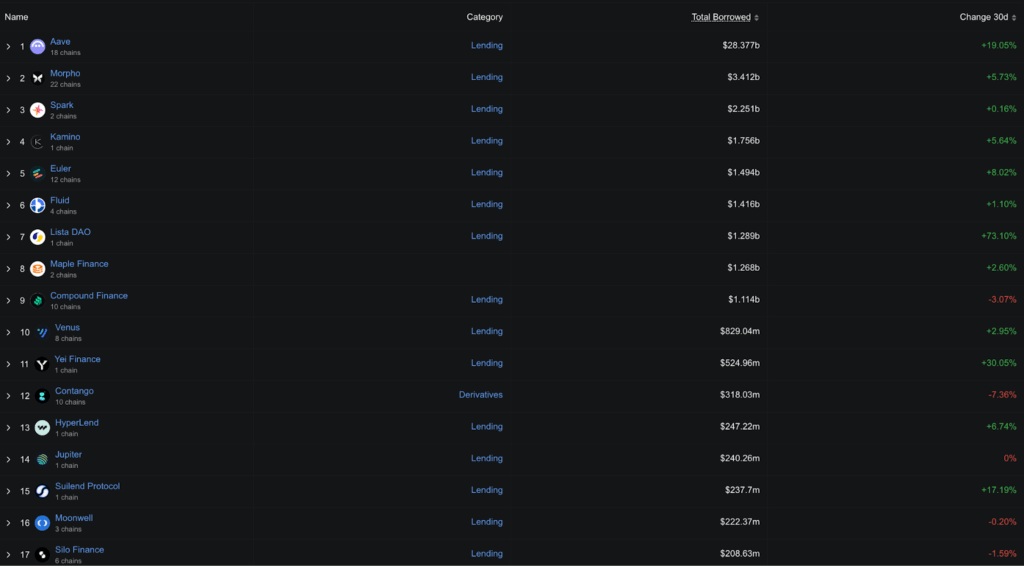

Aave dominates the space with $28.3 billion borrowed, nearly 70% of the total, followed by Morpho with $3.4 billion and Spark with $2.25 billion.

Smaller names like Euler ($1.49 billion) and Fluid ($1.41 billion) are also gaining traction, with Lista DAO seeing the sharpest growth, up 73% over the past month.

Deposits into lending protocols are even higher, sitting around $70 billion in total. This shows that while borrowing demand is rising, there is still plenty of idle liquidity waiting.

A Savings Account for Some, Leverage for Others

For depositors, lending now works like a simple savings account. Returns vary by platform and asset. For example:

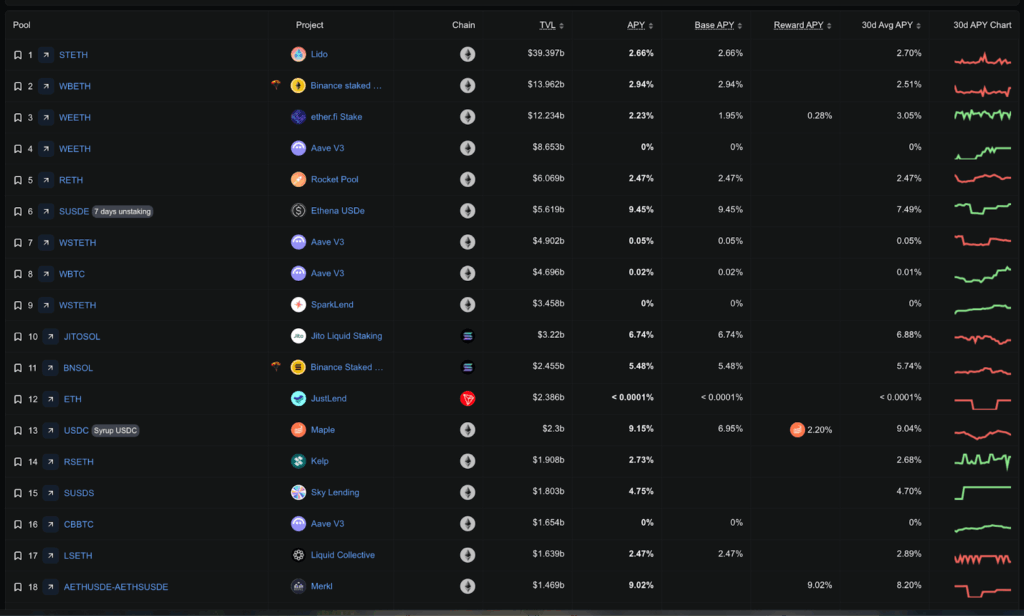

Lido’s stETH pool, with nearly $40 billion locked, pays around 2.66% APY. Also, Binance’s WBETH pool, worth $13.9 billion, pays about 2.94% APY. One of the reasons why Binance might be seeing a stablecoin surge!

Ethena’s USDe, though smaller at $5.6 billion, pays one of the highest yields at 9.45% APY. That explains why the native token, ENA, has been moving higher.

For users, these percentages turn into real income. A depositor putting $10,000 into lending can make between $200 and $900 a year, depending on the platform.

On the other side, borrowers pay more. Depending on the token, the cost to borrow runs between 5% and 9% a year.

This is the bridge that links savers and traders — one group earns steady interest, the other takes on debt to try and profit in the markets.

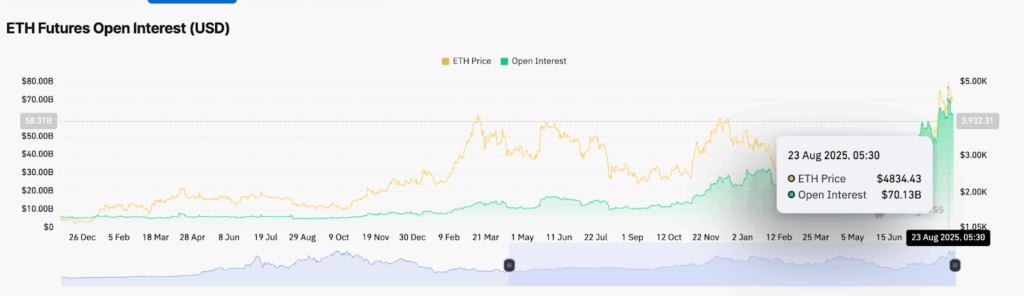

The effect shows up in trading data. Even while Bitcoin and Ethereum prices have stayed flat, open interest in futures and other derivatives has climbed.

That means much of the borrowed money is going into leveraged bets rather than simple spot buying.

Big lending platforms are the main winners from this trend. AAVE is the leader with more than $28 billion borrowed, while smaller players like Morpho and Spark are also growing.

The point is simple: crypto is not only about buying and selling coins anymore.

For many people, DeFi lending now works like a savings account. They deposit stablecoins and earn steady interest, usually between 2% and 9%.

On the other side, traders borrow this money to place bigger bets, often in derivatives markets.

These two groups, savers and traders, keep the system balanced. Together, they are turning DeFi lending back into one of the most active areas in crypto.