Lululemon Stock Nosedives 20%—Because Beating Earnings and Crushing International Sales Just Isn’t Enough

Wall Street delivers another masterclass in irrationality: Lululemon posts strong Q1 numbers with international growth, and the stock gets punished like a yoga mat after hot power vinyasa.

Here’s the breakdown:

The Good (That Somehow Didn’t Matter)

Earnings beat expectations. International sales surged. The kind of performance that—in a sane world—would trigger confetti cannons on the trading floor.

The Bad (The Only Thing That Mattered)

Investors dumped shares anyway, slicing over 20% off the price. Maybe they were distracted by shiny AI stocks, or just adhering to the golden rule of modern markets: good news = sell opportunity.

The Ugly Truth

Another reminder that fundamentals are just suggestions when algorithms and momentum traders run the show. But hey—at least the shorts got a free athleisure outfit today.

TLDR

-

Q1 2025 revenue rose 7% to $2.4 billion, EPS of $2.60 beat expectations

-

Gross margin improved by 60 basis points to 58.3%

-

U.S. market saw only 2% revenue growth, weighing on investor sentiment

-

Company repurchased $430 million in shares; store count reached 770

-

FY25 EPS outlook cut despite maintaining revenue forecast

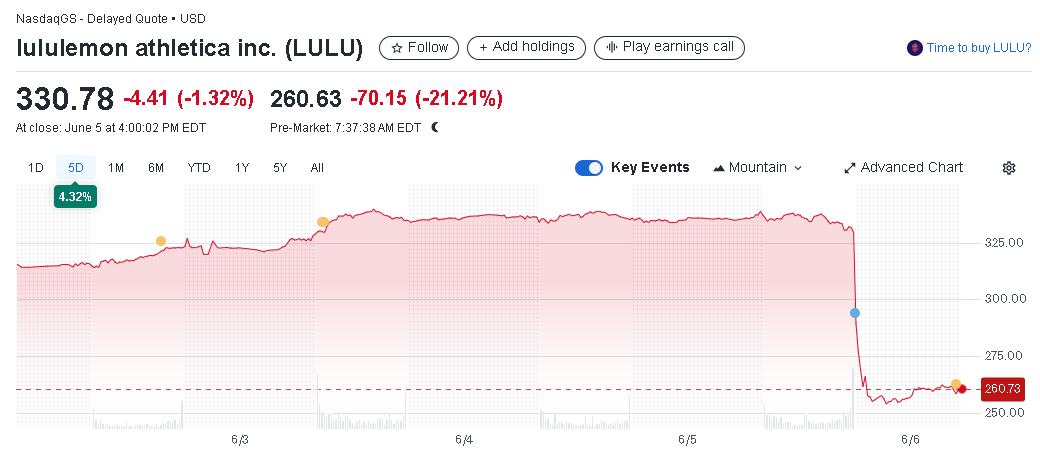

On June 5, 2025, Lululemon Athletica Inc. (NASDAQ: LULU) reported its Q1 2025 results, posting revenue of $2.4 billion, a 7% year-over-year increase, or 8% on a constant currency basis. Diluted earnings per share came in at $2.60, ahead of Wall Street estimates. Despite the beat, shares closed at $330.78 and plunged 21.23% in pre-market trading to $260.57 as investors reacted to margin pressures and weak growth in the Americas.

Lululemon Athletica Inc. (LULU)

Gross profit increased 8% to $1.4 billion, and gross margin improved by 60 basis points to 58.3%, aided by lower product costs and improved markdowns. Operating income stood at $438.6 million, but the operating margin declined to 18.5% from 19.6% in Q1 2024. SG&A expenses increased to 39.8% of net revenue, up from 38.1% a year earlier, impacted by FX losses.

lululemon athletica inc., $LULU, Q1-25. Results:

🔴 -12% Post-Market 🚨

📊 Adj. EPS: $2.60 🟢

💰 Revenue: $2.37B 🟢

📈 Net Income: $314.6M

🔎 International markets drove strong growth, up 19%, offsetting softness in U.S. sales. pic.twitter.com/E3LsaQE4VZ

— EarningsTime (@Earnings_Time) June 5, 2025

Americas Soft, China and International Growth Strong

Lululemon’s U.S. performance lagged as revenue grew just 2%, reflecting cautious consumer behavior. Comparable sales in the Americas dropped 2%, or 1% on a constant dollar basis. In contrast, international markets delivered robust results. Revenue in China Mainland jumped 21%, or 22% in constant currency, while the Rest of World segment saw growth of 16% to 17%.

International comparable sales increased 6%, supporting Lululemon’s strategic push beyond North America. CEO Calvin McDonald noted strength across channels and markets, with strong brand engagement and product innovation globally.

Inventory and Store Expansion

Lululemon ended the quarter with 770 stores after adding three new outlets. Inventories ROSE 23% year-over-year to $1.7 billion, with a 16% increase on a unit basis. Cash and cash equivalents stood at $1.3 billion, and the company repurchased $430 million worth of shares during the quarter, indicating management’s confidence in long-term growth.

Cautious Full-Year Outlook

Despite Q1 strength, Lululemon cut its full-year EPS guidance to $14.58–$14.78, citing expected margin pressure from tariffs and markdowns. The company maintained its revenue forecast at $11.15–$11.30 billion, implying 5% to 7% growth. Q2 revenue is projected between $2.535–$2.560 billion with EPS in the range of $2.85–$2.90.

Operating margin is expected to decline 160 basis points for the full year, driven by elevated tariffs and costs. CFO Meghan Frank emphasized the company’s focus on executing strategy with discipline amid a challenging macroeconomic backdrop.

Long-Term Stock Performance Lags S&P 500

Despite a strong brand and global expansion, Lululemon’s long-term returns have underwhelmed. Year-to-date, LULU is down 13.5%, and over five years, it’s returned only 3.44%, compared to the S&P 500’s 85.96%.