Wall Street Resets Amazon Stock Target as AWS AI Demand Surges: Analysts See 40% Upside

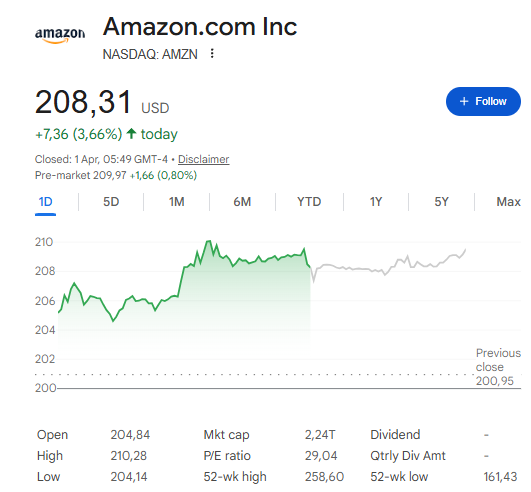

Major Wall Street institutions are sounding the alarm on Amazon's valuation gap, warning that a 10% year-to-date correction has created a critical divergence between its current share price and surging analyst targets. Citi and JPMorgan have aggressively lifted their Amazon stock target to $285, citing explosive AWS AI demand as the primary catalyst, with consensus now pointing to a staggering 40% upside from current levels. The entire 2026 forecast hinges on whether AWS can sustain its growth trajectory to justify the company's massive capital expenditure cycle, setting the stage for a pivotal market re-rating.

Amazon Stock Forecast 2026 As AWS AI Demand Drives Growth

AWS Reaccelerates and Analysts Raise the Amazon Stock Target

AWS grew 24% year-over-year in Q4 2025, hitting $35.6 billion in revenue — the fastest quarterly pace in 13 quarters — while operating margin held at 35%. Citi now expects Amazon AWS growth to reach 28%–29% in 2026, then jump to 37% in 2027 as the Anthropic and OpenAI partnerships scale further. Custom chips, Trainium and Graviton specifically, already generate over $10 billion in annual revenue and add another real layer to the AWS AI demand case that analysts keep pointing to.

CEO Andy Jassy stated:

“I’ve been thinking for the last number of years that AWS, call it 10 years from now, could be about a $300 billion annual revenue, run rate business.”

Evercore ISI analyst Mark Mahaney, who named Amazon his top internet pick for 2026, said:

“At the end of the day, Amazon remains a high quality compounder (25% EPS compound annual growth rate), with solid double-digit revenue growth, expanding operating margins, and free cash flow likely to inflect up materially in a 24-month timeframe.”

What the Spending Cycle Means for the Amazon Stock Target

Amazon plans to spend around $200 billion in capex in 2026, up from $131.8 billion in 2025 and $83 billion in 2024. That spending hit free cash flow hard — it dropped 70% year-over-year to $11.2 billion in 2025, even as operating cash flow climbed 20% to $139.5 billion. The Amazon stock price prediction at current levels factors in the idea that AWS and advertising — which grew 23% year-over-year to $21.3 billion in Q4 2025 — together cover that pressure as returns start coming through. Analysts also treat Amazon AWS growth and the advertising flywheel as two separate reasons to stay bullish on the Amazon stock price prediction.

JPMorgan analyst Doug Anmuth, who carries a $285 Amazon stock target, said:

“Amazon is the most diversified mega-cap across revenues and profit and has various large growth opportunities — mixed sentiment and attractive valuation.”

Anmuth also flagged Amazon’s $38 billion, seven-year cloud deal with OpenAI as something that could “add upside” to the company’s top line — a detail that analysts across the Street keep coming back to in the Amazon stock forecast 2026 conversation. The Amazon stock target range of $250–$305 across major firms tells you that confidence in the growth story is high right now, and most of that confidence ties back to AWS AI demand and where Amazon AWS growth goes from here.