Paper Gold vs Paper Bitcoin: Do ETFs Undermine the Real Deal?

ETFs promise exposure without ownership—but at what cost?

Gold's glitter fades as Bitcoin ETFs flood the market

Wall Street's latest paper game: slicing crypto into tradable IOUs

When your 'digital gold' ETF gets rehypothecated three times over

Trustless assets? Maybe. Trust-heavy financial products? Absolutely.

Bonus jab: Nothing says 'innovation' like repackaging assets into fee-generating vehicles for middlemen.

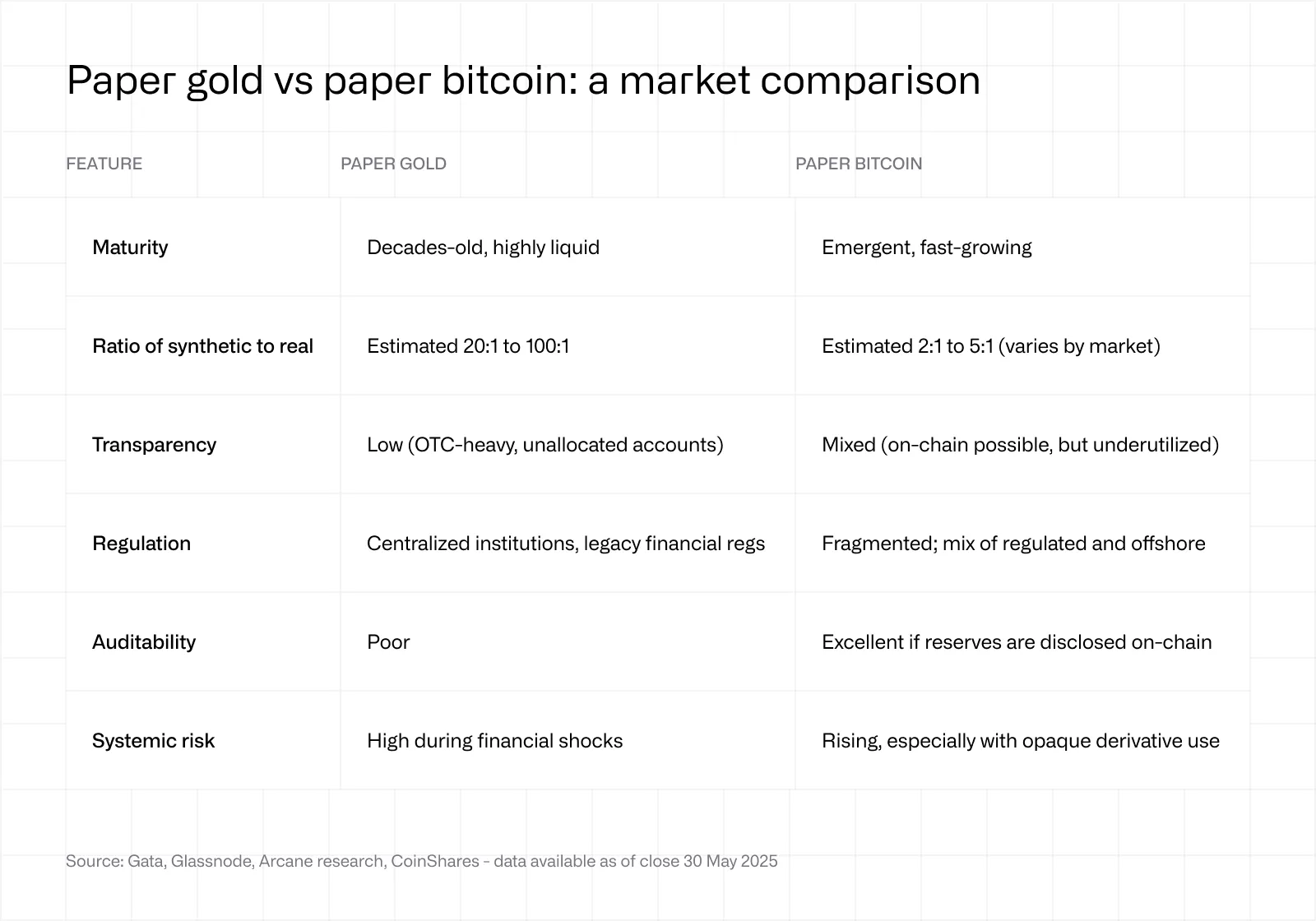

Paper gold: The analogy

To understand this concern, we must revisit the history of "paper gold." Originating with special drawing rights in the 1960s, the term now refers to financial products that provide Gold exposure without requiring physical possession. These include ETFs, futures contracts, and shares of gold mining firms. While convenient and liquid, these instruments introduced counterparty risks and obscured how much physical gold was actually backing them.

Over time, the majority of gold trading moved into opaque over-the-counter markets, particularly in London. According to the World Gold Council, over 70% of wholesale gold trades happen off-exchange, with limited public insight. And unlike Bitcoin’s 21 million cap, gold’s total supply-including what’s still in the ground-remains speculative.

Paper bitcoin: The growing concern

Bitcoin, often dubbed "digital gold," is increasingly adopting similar financial structures: futures, options, ETFs, and custody-based exposure mechanisms. While these instruments offer broader access, they can also detach investors from the underlying asset-especially if issuers aren't fully transparent.

The term "paper bitcoin" gained traction when accusations surfaced in September 2024. Coinbase, custodian for multiple Bitcoin ETFs including BlackRock's iShares Bitcoin Trust, was alleged to have issued IOUs rather than holding real bitcoin. Though Coinbase CEO Brian Armstrong denied these claims and Adam Back publicly debunked them, the event sparked industry-wide concern.

The assumption of “paper bitcoin” has gained traction on social channels, often based on the perception that it’s abnormal for Bitcoin’s price to remain range-bound despite the growing number of Bitcoin treasury companies and the rapid expansion of Bitcoin ETFs. According to this view, increased institutional exposure should translate directly into stronger upward price momentum.

However, this assumption is flawed, as Bitcoin’s supply dynamics are governed by complex mechanisms: price action is not driven solely by inflows into ETFs or balance sheet allocations. It also depends on factors such as market liquidity, derivatives positioning, macroeconomic sentiment, miner behavior, and long-term holder activity. Additionally, not all ETF inflows result in immediate spot purchases: some issuers hedge exposure using futures or rely on internal market-making structures, which can dilute the expected price impact.

Understanding Bitcoin’s market structure requires looking beyond headline flows and considering the layered interaction between spot, derivatives, and custody markets.

Nonetheless, If "paper bitcoin" proliferates without robust verification, we risk returning to a world where market participants can't confidently verify whether assets are backed 1:1, which WOULD contradict Bitcoin's founding ethos.

Proof of reserves: Tool or illusion?

Following FTX's collapse in 2022, the industry championed proof of reserves (PoR) as a safeguard. At its best, PoR confirms that a company holds assets it claims to, ideally matched against liabilities. But proof of reserves can also be a smoke screen, since reserves can be temporarily inflated before audits and there are no industry standards to properly release the proof. Take crypto exchanges: unless a user is able to verify an exchange’s deposits on its deposit address in real time, the use of fractional reserves might be a reality. Delayed withdrawals also constitute a warning signal.

When it comes to publicly listed Bitcoin treasury companies, one could lament that - Metaplanet aside - none of them provide a way to independently verify their holdings as of the time of writing.

It is important to highlight that, on another note, publicly-traded products and funds issuers are covered by legacy financial regulations and are subject to the reporting requirements enforced by listing venues.

The Adam Back rebuttal

When the September 2024 rumor storm hit, Adam Back, a Bitcoin pioneer, quickly countered the narrative, stating there's no evidence Coinbase issued unbacked IOUs. His comment served as a reminder: skepticism must be data-driven, not social-media fuelled. But the scare reinforced one point: perception matters as much as fact when it comes to market trust.

Nonetheless, all rumours circulating on the internet and social channels should be taken with nuance. In 2024, Bloomberg ETF analyst Eric Balchunas emphasized that after covering the industry “for 20 years, there’s never been a case of this stuff [the underlying asset]not being with the custodian.”

Moreover, it is important to remember that disclosing holdings is more complex than simply displaying a public address - especially because doing so exposes the address to spam attacks such as dusting, a tactic in which malicious actors send assets to your address without consent. These assets can, for instance, be tainted.

Yet, Bitcoin offers something no other asset can: full transparency. But this promise is at risk if we allow financial engineering to outpace verification. Investors should demand more than convenience: they should demand cryptographic certainty.

The threat of "paper bitcoin" is real, but avoidable. By holding institutions accountable, promoting best practices, and embracing the tools that blockchain provides, we can ensure that Bitcoin remains what it was always meant to be: trustless, auditable, and radically transparent.