Citrini Research Issues Massive Buy Alert: Solana, Ethereum L2s, and XRP Primed for Surge

Institutional analysis firm Citrini Research just flashed a major bullish signal across the crypto board—and it's pointing squarely at high-throughput blockchains and scaling solutions.

The Scalability Play Gets a Green Light

Forget the noise. The latest deep-dive report cuts through market chatter to highlight a fundamental shift. The data suggests infrastructure built for speed and lower costs—like Solana and Ethereum's Layer 2 networks—is entering a prime adoption phase. It's a classic case of technology catching up to promise, while legacy systems grapple with congestion fees that would make a traditional banker blush (though they'd probably just pass the cost along to clients).

Where the Smart Money is Looking

The signal isn't just broad; it's specific. Analysis of on-chain activity, development velocity, and capital flow patterns reveals concentrated strength. The narrative is moving beyond mere store-of-value to utility and scale. This positions the assets with proven throughput and active ecosystems directly in the crosshairs of the next wave of institutional allocation.

One cynical take? The 'huge buy signal' might just be the sound of funds rotating out of overhyped narratives and into platforms that actually work. The market has a funny way of rewarding utility—eventually.

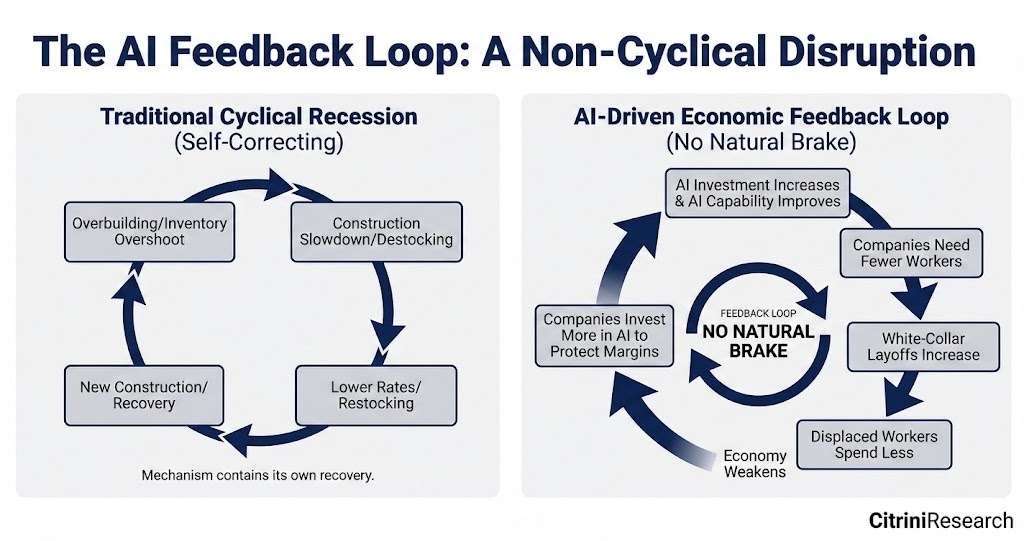

Entering an age of abundant intelligence

There is no self-correction as we WOULD expect to see in a typical cyclical recession.

It goes something like this: construction (or other economic activity) slows, rates adjust downwards, allowing businesses to return to expanding output, until overproduction kicks in again, and so on.

In the AI doom loop, AI improves, fewer workers are needed, fewer workers mean less spending, the economy weakens, companies invest in more AI to protect margins, AI gets even better, and the cycle repeats – there is no natural break.

We thought it was a sectoral story. I’m not in Software-as-a-Service (SaaS), so there’s no need to worry. But it is more than software. Much more. It was a comforting notion that AI would usher in an era of creative destruction, as seen in past technological assaults on the old ways of doing things.

Yes, AI will destroy jobs, but, as in the past, new jobs and hitherto unimagined industries would emerge to replace them.

Trouble is, according to Citrini’s scenario, AI is a story of human intelligence displacement. The entire white collar workforce is imperilled. It is the consequence of abundant intelligence.

The authors of the Cetrini report remind us that advanced economies like the US are service-based. The report breaks that down so everyone can understand:

“The US economy is a white-collar services economy. White-collar workers represented 50% of employment and drove roughly 75% of discretionary consumer spending. The businesses and jobs that AI was chewing up were not tangential to the US economy, they were the US economy.”

Unfortunately for all of us – white collar, blue collar, whatever – machines don’t buy stuff.

AI agents destroy intermediation – bye bye credit cards, hello stablecoins

The report makes a robust case for how consumer agents will end the age of intermediation.

AI agents operate autonomously on behalf of their human owners, which means they can find the best flight or hotel on the market with ease because they never get tired, don’t find anything monotonous or dull, and never sleep.

![]() BIG WARNING: AI COULD PUSH GLOBAL ECONOMY INTO A RECESSION THIS DECADE.

BIG WARNING: AI COULD PUSH GLOBAL ECONOMY INTO A RECESSION THIS DECADE.

And this will not happen by AI bubble burst, but rather by AI becoming bigger and better.

This is a scenario laid out by Citrini in their report, and here's why you should pay attention:

Right now, AI is… pic.twitter.com/FIu9PsZA2X

The days of companies relying on our laziness or inertia are numbered. Add ‘vibe coding’ to the mix, and a new wave of startups can spin up delivery services apps in a few weeks to compete with DoorDash et al, or automate workflow in a bespoke way that fits your corporate needs more performantly than say Monday. Everywhere, fees are being compressed to NEAR zero.

And then we come to our friends, the banks. Why pay fees to Mastercard and Amex when you can use a stablecoin running on a low-fee blockchain like Solana, or an Ethereum Layer 2 like Base, Arbitrum, Optimism, or Polygon?

“Once agents controlled the transaction, they went looking for bigger paperclips.

“There was only so much price-matching and aggregating to do. The biggest way to repeatedly save the user money (especially when agents started transacting among themselves) was to eliminate fees. In machine-to-machine commerce, the 2-3% card interchange rate became an obvious target.

“Agents went looking for faster and cheaper options than cards. Most settled on using stablecoins via solana or Ethereum L2s, where settlement was near-instant and the transaction cost was measured in fractions of a penny.”

And what agentic AI will do for stablecoins could also be applied to cross-border payment protocols like Ripple’s XRP Ledger, although it doesn’t get a mention in this report.

Coinbase has already begun experimenting with a protocol that allows AI agents to make payments on-chain.

The tokenization, disintermediation, agentic AI narrative to beat the bear market blues

Crypto has been looking for a “new” narrative to lift the fog of the bear market. Well, it’s been hiding in plain sight: tokenization, disintermediation, and Agentic AI.

Will that solve the problem of an economy without enough workers getting paid wages and salaries to drive the consumption that companies depend on?

Probably not, but as the report contends, we’ve got time to figure out a solution for that. Taxing the hyperscaler ‘robber barons’ is suggested, but that’s unlikely to go down well with the Lords of the data centers.

In payments, as elsewhere, disruption is coming and everyone – investors, companies, and consumers – needs to start thinking about what it all means.

Consumer behavior is already shifting. Chargebacks911, a global leader in dispute resolution and chargeback prevention, is warning merchants and payments firms that agentic commerce will reshape disputes, as AI systems MOVE from recommending purchases to executing them. Chargebacks are payment reversals initiated by a cardholder’s bank.

For years, most chargebacks fell into three categories: fraud, merchant error, or buyer’s remorse. Agent-initiated transactions create a fourth scenario. The purchase is technically authorised, but the result does not match the customer’s expectations.

“The payments industry has always treated the click as the signal of intent,” says Monica Eaton, founder and CEO of Chargebacks911.

“Agentic commerce removes the click. So now we need a new way to prove intent when a human was not directly involved.”

Keep an eye on your bank account, and welcome to the future.

Report co-author Alap Shah, explains more about the ideas in the report, such as AI-induced ‘ghost GDP’, where value accrues on the balance sheets of the hyperscalers but does not show up in the “human-centric consumer economy”: