Standard Chartered Sounds Alarm: Are Stablecoins Quietly Draining Traditional Banks?

Forget the flashy headlines about Bitcoin's volatility—the real financial revolution might be happening in plain sight, with stablecoins quietly rerouting capital flows away from traditional banking systems.

Banking's Silent Drain

Major financial institutions are starting to notice a persistent, low-level hum. It's the sound of capital migrating from conventional savings and transaction accounts into dollar-pegged digital assets. This isn't about speculative crypto plays; it's about efficiency, speed, and often, a better yield than what's offered on the high street. These programmable tokens bypass legacy settlement layers, offering near-instant, cross-border transactions 24/7. Why wait three days for a wire when a stablecoin transfer settles in seconds?

The Institutional Whisper

The concern voiced by Standard Chartered isn't about a bank run tomorrow. It's about a gradual, structural shift. As tokenization of real-world assets gains steam, stablecoins become the default settlement rail. Every corporate treasury that opts for a digital dollar balance over a traditional bank deposit represents a quiet outflow. It's death by a thousand cuts—each one justified by lower fees and superior technology.

Provocative but Balanced Closer

This isn't a prophecy of doom for banks, but a stark wake-up call. They can either innovate their plumbing to compete with the seamless flow of decentralized finance, or watch their most valuable resource—liquidity—slowly seep into a more efficient system. After all, in finance, capital flows to where it's treated best—even if that means trading a vault for a cryptographic key. The cynical jab? Banks spent decades building moats; they just never expected the competition to build faster boats.

Stablecoins Test Traditional Banking as Adoption Accelerates

Geoff Kendrick, Standard Chartered’s global head of digital assets research, said the growing role of dollar-pegged tokens threatens to redirect funds into the digital asset ecosystem, particularly if upcoming U.S. legislation provides clearer regulatory footing.

![]() Clear Street analyst says blockchain adoption is advancing even without U.S. regulatory clarity — but warns the Clarity Act risks protecting bank margins over crypto innovation.#Blockchain #ClarityActhttps://t.co/Nw8Xcyvq3X

Clear Street analyst says blockchain adoption is advancing even without U.S. regulatory clarity — but warns the Clarity Act risks protecting bank margins over crypto innovation.#Blockchain #ClarityActhttps://t.co/Nw8Xcyvq3X

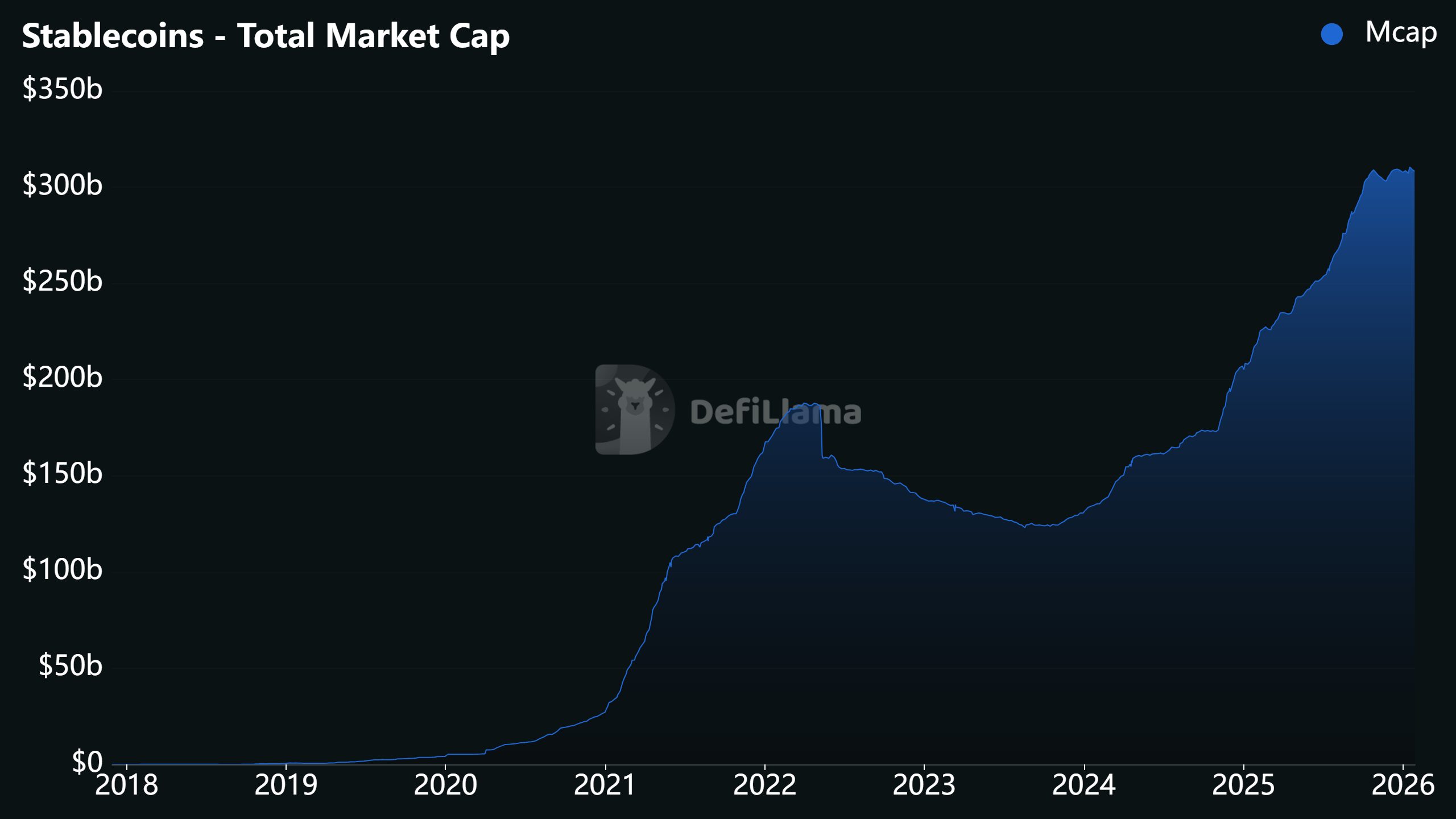

The numbers behind the concern are already taking shape. Stablecoin supply has climbed more than 40% over the past year to just over $300 billion, according to DefiLlama data.

Standard Chartered estimates that U.S. bank deposits could fall by roughly one-third of total stablecoin market capitalization, with growth expected to accelerate if Congress passes the proposed CLARITY Act.

The issue goes beyond payments alone. Kendrick noted that stablecoins are increasingly touching Core banking functions, from transaction settlement to liquidity management.

At the same time, a central point of tension between banks and crypto platforms is whether consumers should be allowed to earn rewards on stablecoin balances.

Coinbase currently offers about 3.5% in rewards on holdings of Circle’s USDC, a practice banking lobby groups argue could encourage deposit flight by making crypto balances more attractive than traditional accounts.

Coinbase CEO Brian Armstrong has publicly pushed back on that argument, saying banks are attempting to use regulation to block competition rather than protect consumers.

![]() Coinbase CEO @brian_armstrong said the exchange cannot support the Senate’s crypto bill as written, warning it WOULD hurt tokenized equities, DeFi and privacy while weakening the CFTC.#Coinbase #CryptoPolicy https://t.co/kMbxepaWYk

Coinbase CEO @brian_armstrong said the exchange cannot support the Senate’s crypto bill as written, warning it WOULD hurt tokenized equities, DeFi and privacy while weakening the CFTC.#Coinbase #CryptoPolicy https://t.co/kMbxepaWYk

Standard Chartered Points to Deposit Sensitivity at Regional Lenders

Standard Chartered’s analysis focused on net interest margin income as a share of total revenue, a metric closely tied to deposits. On that basis, regional U.S. banks appear more exposed than larger, diversified institutions.

Among the 19 banks and brokerages reviewed, Huntington Bancshares, M&T Bank, Truist Financial, and Citizens Financial Group were identified as the most vulnerable.

Regional lenders rely more heavily on deposits to fund loans, meaning even modest outflows could have an outsized impact.

For now, markets suggest the threat is not immediate. U.S. bank deposits have rebounded after sharp declines in 2022 and early 2023, reaching a record $18.72 trillion in December 2025.

Core deposits grew by about 4% in 2025, up from 1.5% the year before, supported by Federal Reserve rate cuts and a slowdown in quantitative tightening.

Bank shares have also held up, with the KBW Regional Banking Index rising nearly 6% in January, compared with just over 1% for larger banks.

Treasury-Backed Stablecoins Add New Twist to Deposit Debate

Still, Standard Chartered’s global head of digital assets research, Geoff Kendrick, argues that the longer-term shift is difficult to ignore. If stablecoin market capitalization reaches $2 trillion, he estimates deposit losses could approach $500 billion.

He also pointed out that reserve practices limit any recycling of funds back into the banking system.

Tether and Circle, the two dominant issuers, hold just 0.02% and 14.5% of their reserves in bank deposits, meaning most backing assets sit in Treasury bills rather than traditional accounts.

Not everyone agrees that stablecoins pose a destabilizing threat. In a recent Bloomberg opinion piece, historians Niall Ferguson and Manny Rincon-Cruz argued that fears of deposit flight are overstated.

![]() Stablecoins top $284B, but economists say deposits and digital assets grow together, showing banks remain stable despite rapid crypto adoption. #Stablecoins #Banking https://t.co/8zDEuJblTS

Stablecoins top $284B, but economists say deposits and digital assets grow together, showing banks remain stable despite rapid crypto adoption. #Stablecoins #Banking https://t.co/8zDEuJblTS

Since USDC launched in 2018, U.S. bank deposits have increased by more than $6 trillion, while stablecoins have grown by about $280 billion.