US Government Confiscates 127,195 Bitcoin from Chen Zhi Scam - Now Controls Over 316K BTC in Treasury

Federal authorities just pulled off one of the largest crypto seizures in history - grabbing 127,195 Bitcoin tied to the infamous Chen Zhi pyramid scheme.

The Government's Growing Crypto Stash

With this massive haul, Uncle Sam's digital wallet now bulges with over 316,000 BTC. That's enough Bitcoin to make any Wall Street hedge fund manager blush - if they understood what they were looking at.

From Fraud to Federal Reserve

The seized coins represent ill-gotten gains from Chen Zhi's investment scam, now finding a new home in government custody. Because nothing says 'justice' like the feds becoming one of the world's largest Bitcoin whales.

Another day, another reminder that while crypto promises decentralization, the government still holds the keys when it wants to.

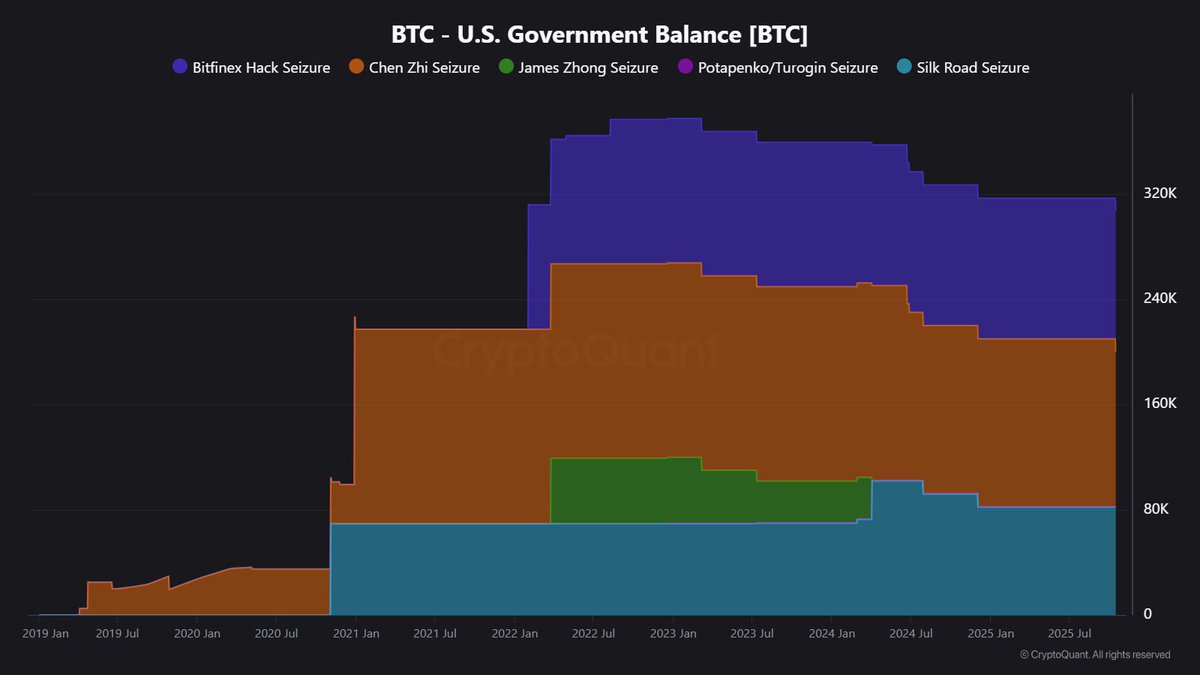

US Government’s Bitcoin Holdings Grow After Historic Seizure

CryptoQuant reports that the US government now controls 316,760 BTC, worth roughly $35.9 billion, following its latest seizure from Chen Zhi’s “pig butchering” scam. The 127,195 BTC confiscated in this case alone—currently valued at $13.2 billion—marks the largest single Bitcoin seizure ever conducted by the Department of Justice. At Bitcoin’s peak earlier this year, those same holdings were worth around $15.5 billion.

This operation cements the US as one of the largest known Bitcoin holders, with its wallet comprising assets from several major law enforcement actions over the past decade. The most significant components include:

Bitfinex Hack (2016) — Law enforcement recovered 106,910 BTC stolen from the crypto exchange after a multi-year investigation. The funds were linked to Ilya Lichtenstein and Heather Morgan, who laundered billions before being arrested in 2022.

Silk Road (2013) — The government confiscated 81,988 BTC from the dark web marketplace operated by Ross Ulbricht. This remains one of the earliest and most famous crypto seizures.

Potapenko/Turogin (2022) — A smaller seizure of 667 BTC connected to Estonian nationals accused of running a $575 million crypto fraud through shell mining services.

Together, these seizures highlight how the US has quietly become a major Bitcoin whale—a position gained not through investment, but through relentless enforcement and asset recovery in the digital age.

Bitcoin Holds Support But Faces Resistance Ahead

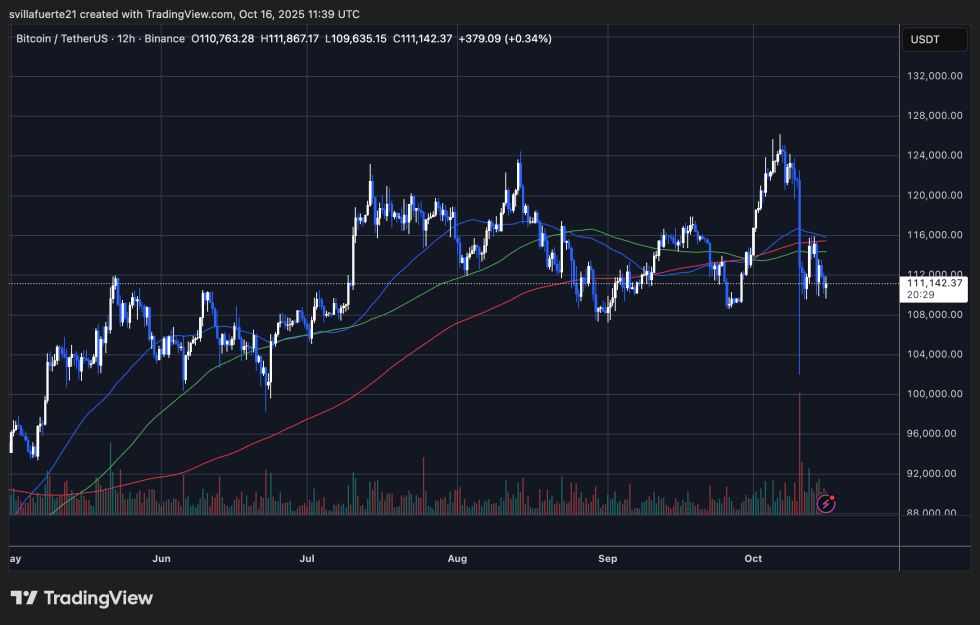

Bitcoin (BTC) is trading around $111,142, showing signs of stabilization after last week’s flash crash that briefly sent prices below $104,000. The 12-hour chart reveals that BTC has found temporary support NEAR the $110,000 zone, which has acted as a key demand area multiple times since mid-September. This range now serves as a battleground between cautious buyers and sellers capitalizing on market weakness.

However, BTC remains below the 50-day (blue) and 100-day (green) moving averages, both currently converging around $114,000–$116,000, creating strong short-term resistance. The 200-day (red) moving average sits near $112,000, slightly above current levels, signaling that the broader trend is still fragile. A clean break above these levels could open the path toward $117,500, but failure to regain momentum may expose BTC to another test of $108,000–$110,000.

Trading volumes remain elevated but slightly cooling compared to last Friday’s capitulation event, suggesting consolidation rather than panic. Overall, Bitcoin appears to be in a recovery phase, though the lack of directional conviction indicates that traders are waiting for stronger catalysts — whether from macro data, ETF flows, or on-chain signals — before taking decisive positions.

Featured image from ChatGPT, chart from TradingView.com