Carnival (CCL) Q3 Earnings Surge: Record Demand Fuels 15% Profit Upside

Cruise giant Carnival defies economic headwinds with blockbuster quarter

Wave of Consumer Spending

Pent-up travel demand crashes through expectations—booking volumes hit unprecedented levels as vacationers splurge on premium experiences. The post-pandemic revenge travel trend shows no signs of slowing, with occupancy rates sailing past pre-crisis benchmarks.

Profit Engine Accelerates

Operational efficiencies and strategic pricing power combine to deliver margin expansion that would make even the most skeptical analyst crack a smile. Higher onboard spending per passenger drives revenue per available cabin beyond projections.

Market Position Strengthens

Competitors watch from distant shores as Carnival's fleet modernization and destination portfolio investments pay dividends. The 15% upside projection reflects not just current performance but sustained momentum through 2026.

Another quarter, another beat—Wall Street's favorite cruise operator continues making traditional vacation stocks look like anchored relics. Maybe they should've invested in blockchain instead.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 55% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

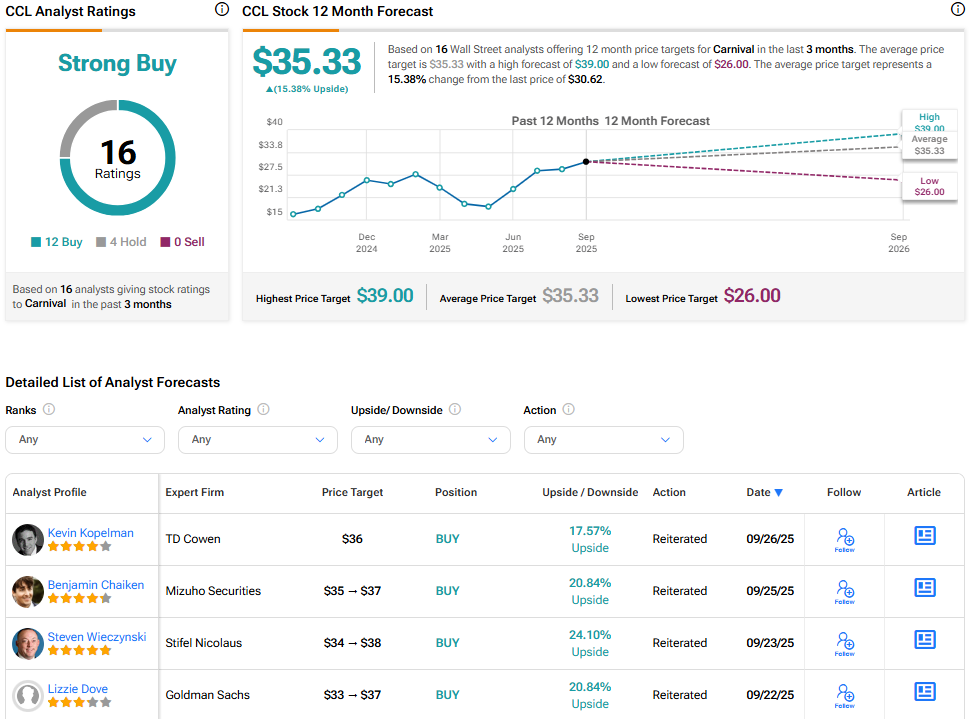

The outlook is supported by strong travel demand and record bookings. Occupancy rates above 112% are seen as a key driver, while firm pricing trends add further support. At the same time, higher costs remain a focus, with analysts pointing to rising cruise operating expenses excluding fuel, along with new destination spending and advertising. In the meantime, CCL shares have climbed a respectable 22% year-to-date.

Analyst View

Several analysts highlight Celebration Key, Carnival’s new private island, as a meaningful growth factor. Mizuho four-star analyst Ben Chaiken raised his target to $37 and reiterated a Buy rating, noting the stock remains compelling as Celebration Key ramps up. TD Cowen’s own four-star analyst Kevin Kopelman set a $36 target with a Buy rating, while Stifel Nicolaus and Goldman Sachs also expect shares to trade in the mid $30s. Overall, sentiment from Wall Street shows continued conviction in Carnival’s growth path.

Focus for Investors

In Q2, Carnival delivered record performance, with net income more than tripling and operating income rising 67%. The company also strengthened its balance sheet by paying down $350 million in debt. Looking ahead, investors will focus on whether Carnival can maintain yield momentum while absorbing higher costs.

Altogether, expectations point to another solid quarter, backed by strong demand and new destination offerings. The key test will be whether Carnival can protect its margins while funding fleet upgrades and new programs.

Is CCL Stock a Buy?

On the Street, analyst sentiment on Carnival Corporation remains positive. Out of 16 recent ratings, 12 are at Buy. The average CCL stock price target is $35.33, which suggests more than 15% upside from the current share price.