Plummeted 55%—Time to Grab The Trade Desk Dip?

The Trade Desk tanks—down a brutal 55% from peak valuation. Market shakes out weak hands as ad-tech faces sector-wide headwinds.

Buying Opportunity or Value Trap?

Numbers don’t lie: a 55% drawdown sparks panic—but also whispers rebound. Bulls see oversold signals; bears scream structural decline. No earnings miss here—just brutal macro sentiment.

Ad-Tech’s Bleeding Edge

Programmatic advertising stalls. Privacy regs bite. Google’s third-party cookie phase-out? Still looming. The Trade Desk’s OpenPath flexes—but can it outmaneuver walled gardens?

Dip Buyers’ Dilemma

Timing the bottom? Risky biz. Averaging down? Smarter—maybe. This ain’t meme stock territory—it’s a fundamentals game. Cash flow strong, client roster solid. But sentiment? Frosty.

Final Takedown

Market veterans smell blood—and opportunity. Retail frets. Hedge funds might already be accumulating. Remember: the market loves to overpunish solid names. Just ask anyone who bought Netflix during its Qwikster flop—then quadrupled their money. Sometimes the best trade is the one that feels worst. Or as Wall Street loves to say: 'Buy when there’s blood in the streets—even if it’s your own.'

Image source: Getty Images

Execution issues and competitive pressures are weighing on The Trade Desk

The Trade Desk started 2025 on a negative note. The stock was clobbered after releasing its full-year 2024 results in February when sales execution issues led the company to miss its revenue target. The company's May quarterly report helped it win back investor confidence as Q1 revenue was up by 25% year over year and well ahead of consensus expectations.

However, inconsistency reared its ugly head once again in Q2. Revenue growth slowed to 19%, and earnings increased just a few cents to $0.39 per share. In the same quarter last year, The Trade Desk had reported much stronger revenue growth of 26%.

The guidance, however, is what really spooked the market. Management expects revenue growth in the current quarter to further decelerate to 14% for a total of $717 million. The adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) forecast of $277 million WOULD be an improvement of just 8% year over year.

It is easy to see why this slowdown has investors worried. The Trade Desk's competitors in the digital advertising market have been reporting solid growth., primarily known for its e-commerce and cloud computing offerings, reported a healthy 23% year-over-year increase in its advertising business last quarter to $15.7 billion.

The tech giant struck a deal with streaming providerto expand its footprint in the connected TV advertising space in the U.S., gaining access to 80 million households. Connected TV is one of the key areas that's driving growth for The Trade Desk, so Amazon's big MOVE in this market is definitely a cause for concern.

On the other hand, social media giant' focus on deploying AI tools is helping it win a bigger share of advertisers' wallets. Meta's tools are driving strong returns for advertisers, and the company has also been able to boost user engagement through AI-recommended content.

As a result, Meta's revenue increased 22% last quarter. It is worth noting that both Meta and Amazon are significantly larger companies than The Trade Desk, and they are achieving healthy growth levels while The Trade Desk is witnessing a slowdown. This doesn't bode well for the company, especially given its valuation.

Why investors could be in for more pain

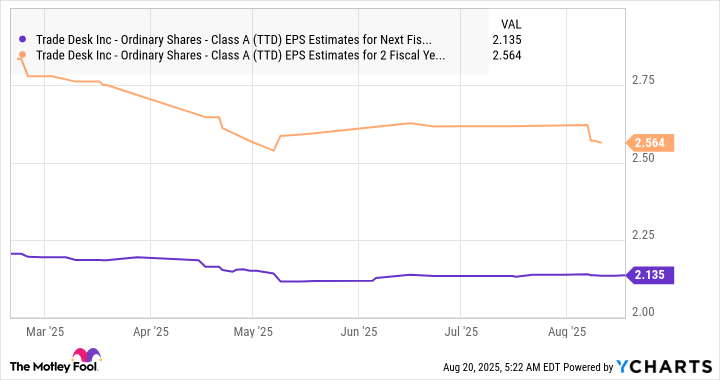

Analysts are forecasting an improvement of just 8% in The Trade Desk's earnings this year to $1.79 per share. The company is expected to return to double-digit growth in 2026.

Data by YCharts.

However, The Trade Desk is trading at 66 times trailing earnings, which is double the average price-to-earnings ratio of the Nasdaq-100 index. Buying The Trade Desk stock at this expensive multiple doesn't look like a smart thing to do right now. The slowing revenue growth is going to negatively impact the bottom line as well, so it remains to be seen if the company is capable of matching Wall Street's earnings expectations going forward.

That's why investors would do well to focus on other tech stocks that are clocking faster growth rates while trading at more reasonable valuations, as The Trade Desk is likely to remain under pressure going forward.