Nvidia Stock: The August 27 Countdown - Buy Now or Brace for Impact?

Nvidia's clock is ticking—and Wall Street's watching every second. August 27 looms like a fiscal cliffhanger, leaving investors scrambling for position.

The AI Gold Rush's Engine

Nvidia isn't just riding the AI wave—it's building the damn servers. Chip dominance fuels everything from data centers to self-driving cars, making its stock a proxy for tech's future.

Timing the Tape

Buying before August 27 means betting on momentum over metrics. Street analysts love the narrative—but then again, they also loved mortgage-backed securities in 2007.

The Verdict: Chip or Dip?

Nvidia either crushes earnings and soars—or becomes another overhyped ticker in the graveyard of 'sure things.' Your move, gamblers.

Image source: Nvidia.

Tech giants are spending record amounts of money on AI data centers

Nvidia's latest Blackwell and Blackwell Ultra GPU architectures have reset the benchmark for the industry. The new Blackwell Ultra GB300 GPU can perform AI inference 50 times faster than Nvidia's previous flagship H100 chip, which is based on the older Hopper architecture. This makes the GB300 ideal for AI reasoning models like OpenAI's GPT-5, Anthropic's Claude 4, and's Gemini 2.5.

According to Nvidia CEO Jensen Huang, reasoning models consume between 100 times and 1,000 times more tokens (words, symbols, and punctuation) than traditional large language models (LLMs), because they spend more time "thinking" in the background to produce more accurate responses.

This is driving incredible demand for the GB300, which will ship in commercial volumes during the second half of 2025. Since Nvidia's fiscal 2026 second quarter included July, investors might receive a detailed GB300 sales update on Aug. 27.

What we know right now is that some of Nvidia's top customers are ramping up their data center spending:

- Alphabet recently increased its calendar-year 2025 capex forecast from $75 billion to $85 billion.

- Meta Platforms recently increased the low end of its 2025 capex forecast from $64 billion to $66 billion, but the company says it could spend up to $72 billion.

- Amazon's 2025 capex could reach a record $118 billion, based on the company's most recent guidance.

- Microsoft's capex hit $88 billion during its fiscal year 2025 (ended June 30), and the company plans to spend even more in fiscal 2026.

Nvidia could report stellar results on Aug. 27

Nvidia's guidance suggests its Q2 revenue grew by 50% year over year, to $45 billion. Based on previous quarters, its data center business is likely to have accounted for almost 90% of that figure, thanks to surging GPU sales.

Wall Street will be eyeing Nvidia's revenue guidance for the third quarter, which is currently underway, because it will reflect the level of demand for its Blackwell and Blackwell Ultra chips. Analysts are looking for a forecast of $52.5 billion (according to Yahoo! Finance), so anything above that will probably be very bullish for Nvidia stock.

At the bottom line, Wall Street's consensus estimate suggests Nvidia delivered earnings of $1 per share during Q2. Earnings typically drive stock prices, so if the official number beats that on Aug. 27, it will be great news for shareholders.

Should you buy Nvidia stock before Aug. 27?

Nvidia stock is up 35% since it reported its financial results for the fiscal 2026 first quarter on May 28, which could be a sign of things to come if its Q2 report meets or exceeds expectations.

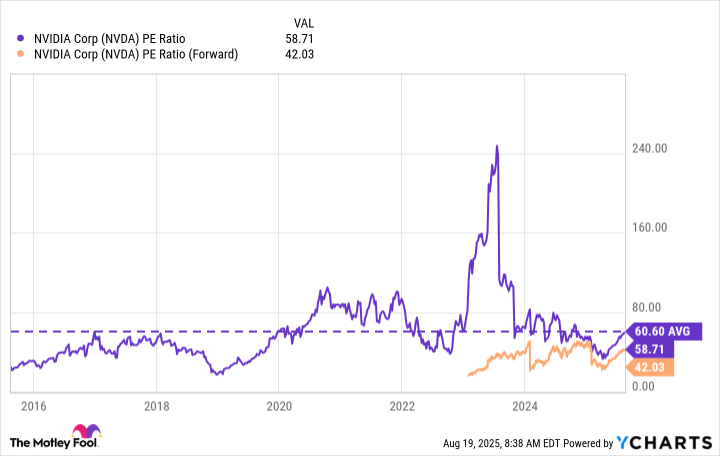

The stock is trading at a price-to-earnings (P/E) ratio of 58.7 as I write this, which is a slight discount to its 10-year average of 60.1, so it's close to fair value. However, Wall Street thinks Nvidia will generate earnings of $4.33 per share during fiscal 2026 overall, placing its stock at a forward P/E ratio of just 42.

That means Nvidia stock WOULD have to climb by 43% over the next six months or so just to trade in line with its 10-year average P/E ratio of 60.1.

NVDA PE Ratio data by YCharts

Therefore, as long as Nvidia's financial results meet analysts' expectations, its stock could be destined for upside following its Aug. 27 report. Since we know many of the company's top customers have increased their capex forecasts, I think the risk that its Q2 results fall short of estimates is very low, so the stock could be a solid buy right now.