SoFi Technologies Stock: 3 Bullish Reasons to Buy Now vs. 2 Bearish Reasons to Hold Off

Fintech disruptor SoFi Technologies is polarizing investors—here’s why the bulls and bears are locked in a tug-of-war.

The Bull Case: Why SoFi Could Skyrocket

1.

Digital banking dominance

: SoFi’s seamless platform is eating traditional banks’ lunch—no brick-and-mortar baggage, just hyper-efficient user growth.

2.

Crypto integration

: While Wall Street dithers, SoFi’s crypto trading features are quietly onboarding millennials who think ‘FDIC’ is a typo.

3.

Student loan rebound

: As the political football gets kicked again, SoFi’s refinancing engine is primed to capitalize on chaos.

The Bear Trap: Why Caution Wins

1.

Regulatory roulette

: The SEC’s caffeine-fueled crackdowns could turn SoFi’s crypto ambitions into a compliance nightmare overnight.

2.

Profitability mirage

: ‘Growth at all costs’ works until your stock chart starts resembling a Celsius Network withdrawal queue.

Verdict? SoFi’s either the next fintech unicorn or a cautionary tale—because nothing screams ‘modern finance’ like betting on unproven disruptors while shorting your own sanity.

Image source: Getty Images.

1. Why buy: Outstanding user growth

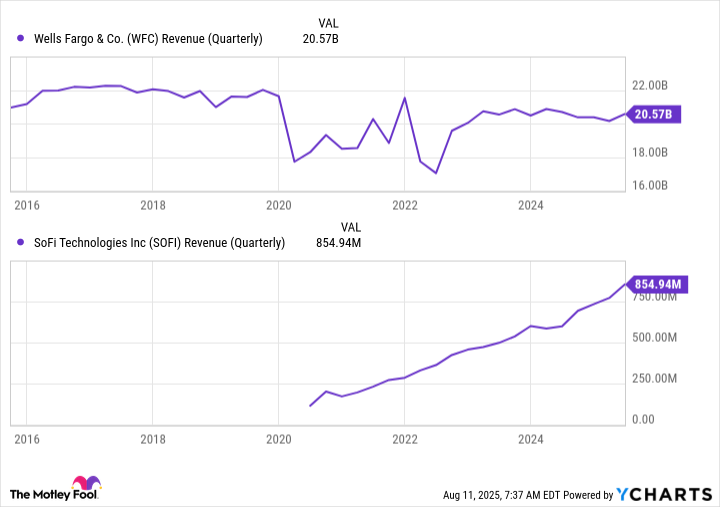

SoFi's bears like to remind investors that consumer banking changes very little over time. While the same basic banking principles apply regardless of the underlying technology, SoFi is attracting new customers at a pace that suggests it has built a unique experience that resonates with American consumers.

SoFi began refinancing student loans in 2012, and didn't launch SoFi Money, the operation that includes basic checking and savings accounts, until 2019. SoFi Technologies acquired a banking license in 2022 and ended that year with 5.3 million members using 7.9 million products. By the end of this June, its business grew to 11.7 million members using 17.1 million products.

To put a little perspective on how difficult it is to get people to switch banks, consider. In 2017, it admitted to creating millions of bogus credit card, checking, and other types of accounts for customers without their consent.

In the years since, Wells Fargo hasn't been as transparent about customer account numbers as SoFi Technologies is now. The publicly traded bank still has to report top-line revenue figures, though. Looking at this metric, the fake account scandal didn't even register.

WFC Revenue (Quarterly) data by YCharts

2. Why buy: Room to continue growing

Many SoFi customers will start with one product, such as a personal loan or checking account. Once they become members, though, getting them to engage with another product like a mortgage, stock brokerage account, or credit card has been relatively easy. In the second quarter alone, SoFi added 1.3 million new products, which worked out to 1.5 products per new customer added during the period.

Investors can likely look forward to more new customers coming on board in the years ahead. Brand awareness recently reached an all-time high, but 91.5% of Americans still haven't heard about SoFi Technologies.

3. Why buy: A consumer bank with fintech chops

In 2020, SoFi acquired Galileo, the technology platform that provides payment processing and other technology support for SoFi's customer-facing applications.

Now that SoFi has its own banking charter, it probably isn't fair to call it a financial technology stock. That said, it's wholly owned technology platform sports more customers than most businesses in the financial technology space.,,and more than 100 other partners rely on Galileo to manage 158 million accounts for their customers.

The Galileo business isn't just a way for SoFi to lower its own technology expenses. Second-quarter revenue from the segment ROSE to $110 million, and plenty of that revenue hits the bottom line. Over the past year, more than 30% of technology segment revenue has been recorded as profit.

The first reason I'm not buying more SoFi stock right now

The last time I purchased SoFi Technologies shares, they were trading at around 2 times the bank's tangible book value. I'd gladly buy more at this valuation, but it's not an option. The stock has been trading at an extremely high 5.5 times its tangible book value.

Well-established consumer banks rarely trade above 2 times their tangible book value. If SoFi's rapid expansion loses steam over the next few years, its valuation could quickly resemble its more-established peers. Although it looks like rapid growth can continue for several more years, this isn't a risk I'm willing to take.

The second reason I'm not adding to my SoFi position now

SoFi is building up its mortgage business, but it mostly relies on unsecured personal loans and student loans for revenue. Credit performance has been pretty good so far. The bank's net charge-off percentage on personal loans fell to 4.5% in the second quarter, or just 2.8% if you account for the delinquent loans it's been able to sell.

Like, SoFi Technologies uses its own system to evaluate individual credit risk. Less reliance on third parties like, the company that sells access to FICO scores, is great for profitability, but this bank hasn't had a real chance to prove itself yet. Americans haven't experienced a long recession in over a decade.

It isn't SoFi's fault that the U.S. economy has been generally strong for an unusually long time. That said, you probably shouldn't buy any up-and-coming lender at a valuation that is more than double that of its established peers unless you're twice as confident about its future credit performance. Over time, I think SoFi can prove itself. For now, it presents more risk than most investors should feel comfortable accepting.