Where to Park $50K in 2025? These Crypto Plays Are Printing Money

Crypto eats Wall Street's lunch—again. While traditional investors chase 5% bond yields, decentralized finance quietly mints new millionaires. Here's how to deploy capital before the next leg up.

ETH: The Blue Chip That Still Runs Hot

Ethereum's Shanghai upgrade finally fixed its gas guzzling rep—now institutions are piling in like it's 2017 ICO season. Staking rewards? A juicy 5.2% APY with zero middlemen.

SOL: The Phoenix Chain

Written off after the FTX crash, Solana's throughput now hums at 2,400 TPS. NFT volumes just reclaimed 90% of their ATH. Contrarians are loading up before the herd notices.

RWA Tokens: T-Bills Go On-Chain

BlackRock didn't tokenize money markets for fun. These yield-bearing stablecoins now command $12B TVL—paying 6.8% while your banker offers 0.01% on savings.

Funny how the 'risky' assets keep outperforming... almost like the whole system's rigged for dinosaurs. Your move, Jamie Dimon.

Image source: Getty Images.

Alphabet

(GOOG 2.44%) (GOOGL 2.48%) is one of the best values in the market right now. It is delivering consistent and strong growth, with revenue and diluted earnings per share (EPS) rising 14% and 22% in the second quarter, respectively.

Normally, that would cause a company like Alphabet to trade at a premium to the market, but that's not the case.

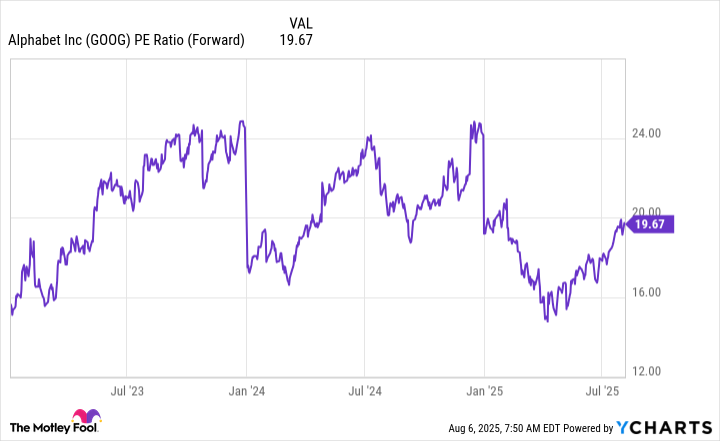

GOOG PE Ratio (Forward) data by YCharts.

Alphabet trades at 19.7 times forward earnings, and the(SNPINDEX: ^GSPC) trades for 23.8 times forward earnings. That's a significant discount to the broader market, and makes Alphabet an excellent stock to buy now before the market bids the stock up.

Meta Platforms

(META 0.92%) delivered a knockout earnings report in Q2. Its revenue was up 22% year over year, despite it only guiding for 13% growth. It expects that strength to continue throughout Q3, with revenue growth expected to be about 20%.

While Meta is investing heavily in building out its artificial intelligence (AI) capabilities, its existing advertising business is thriving. Some of Meta's AI investments are starting to pay off, with AI ad creation becoming more popular and various AI initiatives driving increased interaction and conversion rates on its platforms.

Meta is more pricey than Alphabet at 27.6 times forward earnings, although it has earned that premium with its rapid growth. Meta is growing significantly faster than the market's long-term average (about 10%). It's not that much more expensive, which makes today's price reasonable.

Taiwan Semiconductor

The AI race wouldn't be possible without cutting-edge chip technology from(TSM -0.33%). Taiwan Semiconductor is a chip foundry and produces chips for big-time clients like(NASDAQ: NVDA) and(NASDAQ: AAPL).

Essentially, if a company doesn't have chip production capabilities, it needs to find a supplier for its chip production. Taiwan Semiconductor has risen to become the top option in this field, and has the growth to show for it. In Q2, TSMC's revenue ROSE by 44% year over year in U.S. dollars. Despite its strong growth rate, Taiwan Semiconductor doesn't have a massive valuation like one may expect.

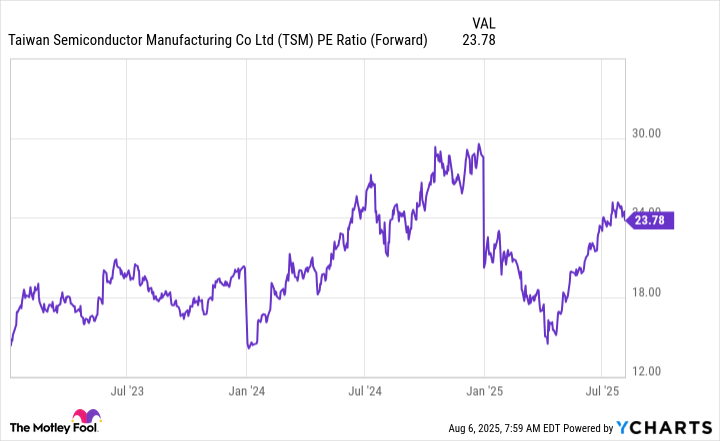

TSM PE Ratio (Forward) data by YCharts.

At 23.8 times forward earnings, it's priced nearly identically to the broader market.

With Taiwan Semiconductor growing at a rapid pace and expected to continue its strong growth for some time, combined with a reasonable price tag, it's an excellent stock to buy now.

Amazon

At first glance,(AMZN -0.23%) looks a bit pricey for its growth and valuation. In Q2, Amazon's revenue increased by 13%, yet it's the most expensive stock on this list at 32.5 times forward earnings.

However, this is the wrong way to look at Amazon's stock. Amazon is an earnings growth story, not a revenue growth story.

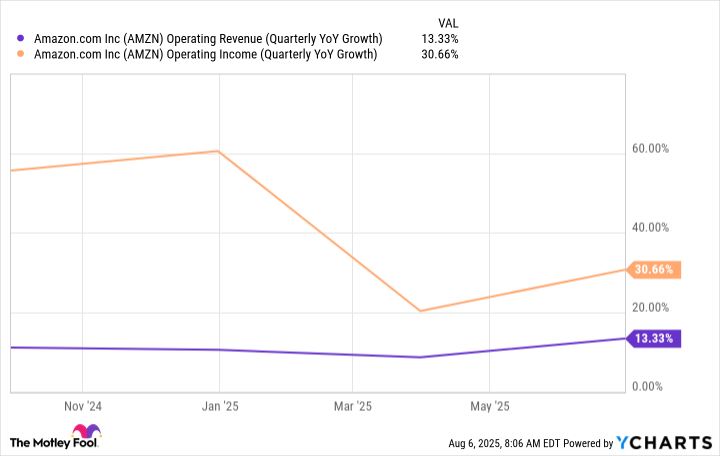

AMZN Operating Revenue (Quarterly YoY Growth) data by YCharts.

Amazon's operating income has been growing at a far faster pace than revenue over the past few quarters. This rise is due to multiple factors, including increased efficiency. But the biggest driver has been from the rise of two segments: Amazon Web Services (AWS) and advertising. Both of these are much higher-margin businesses than the base commerce business Amazon is known for. Additionally, each is growing rapidly, with AWS' revenue rising 17% and advertising service revenue rising 23% in Q2.

This is a long-term trend that will continue for many years, and a patient investor will be well rewarded for sticking with Amazon's stock over the next few years. With the stock reacting negatively following Q2 results, now seems like an excellent time to scoop up shares.