Workday (WDAY) Stock Tumbles Nearly 6% Despite Smashing Analyst Targets

Workday just delivered the numbers Wall Street begged for—and investors responded by dumping the stock. Go figure.

The Earnings Paradox

WDAY beat analyst targets across the board, yet shares plunged nearly 6% in today's session. Because nothing says 'rational market' like punishing companies for exceeding expectations.

Market Mechanics vs. Logic

Traders locked in profits ahead of guidance whispers—typical short-term thinking that overlooks fundamentals. The selloff reflects more about hedge fund algorithms than actual business performance.

When Beating Estimates Isn't Enough

Even stellar earnings can't satisfy the insatiable appetite of institutional traders looking for any excuse to rebalance portfolios. Another day where Wall Street proves it can't see past the next quarterly report.

Maybe the real earnings miss was the market's ability to think long-term.

TLDRs;

- Workday beats analyst expectations with $2.4B revenue and $2.21 EPS but issues flat guidance for Q3.

- Shares fell nearly 6% in after-hours trading as cautious revenue forecasts overshadowed strong Q2 performance.

- CEO Carl Eschenbach cited funding slowdowns in state and local government clients as key growth headwinds.

- Workday shifts hiring overseas, cutting 1,750 jobs in February to manage costs and support AI investments.

Workday (NASDAQ: WDAY) reported stronger-than-expected fiscal Q2 results, posting revenue of $2.4 billion, a 13% year-on-year increase that exceeded Wall Street projections of $2.3 billion.

The finance and HR software provider also delivered adjusted earnings per share of $2.21, beating the forecast of $2.11. Net income climbed to $228 million, up from $132 million a year earlier, underscoring solid operational performance.

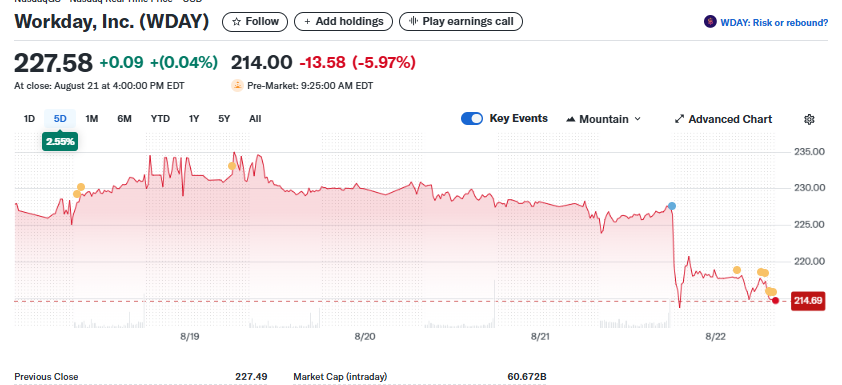

Despite these results, Workday shares dropped nearly 6% in after-hours trading, reflecting investor concerns over its cautious forward outlook. At Tuesday’s close, the stock stood at $227.58, before sliding to $214.00 in pre-market trading the following morning.

Guidance Matches Expectations, Not Investor Hopes

While Q2 results topped expectations, Workday’s guidance for the current quarter came in at $2.4 billion, precisely in line with analyst consensus.

For the full fiscal year, the company reaffirmed revenue guidance of $9.5 billion, again matching but not surpassing Wall Street’s estimates.

This tempered forecast left investors unsatisfied, particularly as competitors in the enterprise software sector have issued more bullish outlooks. Analysts noted that growth deceleration remains a key factor weighing on investor sentiment, especially given Workday’s 12% stock decline year-to-date, compared to a 9% gain for the Nasdaq Composite.

Workday, $WDAY, Q2-26. Results:

📊 Adj. EPS: $2.21 🟢

💰 Revenue: $2.35B 🟢

📈 Net Income: $228M

🔎 Subscription revenue growth of 14% and strong AI-driven platform momentum boosted performance. pic.twitter.com/sxnVNP2P6Y

— EarningsTime (@Earnings_Time) August 21, 2025

Sector Headwinds Challenge Growth

Workday executives pointed to challenges in the state and local government sector, citing slower funding cycles and reduced IT budgets.

CEO Carl Eschenbach highlighted that state-level clients and higher education institutions tied to healthcare systems have been particularly cautious, influenced by federal policy shifts and delays in grant programs such as Title I and Title IV.

The public sector has traditionally been an important market for Workday, but its exposure has become a double-edged sword as budget pressures and funding uncertainties Ripple across education and healthcare-related institutions. These headwinds create uneven revenue visibility, particularly in an environment where governments face tightening fiscal constraints.

Strategic Moves Amid Global Workforce Shifts

Beyond financial performance, Workday continues to adapt its global workforce strategy. In February 2025, the company announced it WOULD cut around 1,750 jobs, focusing on expanding operations in lower-cost international markets like Costa Rica.

The MOVE aligns with broader industry trends, as peers such as Salesforce, PayPal, and ServiceNow pursue international hiring to offset U.S. labor costs while investing in artificial intelligence (AI) initiatives.

Workday’s pricing structure, starting at roughly $99 per employee per month, with large-scale implementations often costing millions, positions it firmly in the enterprise segment. While this ensures high-value contracts, it also slows customer acquisition growth as the company penetrates deeper into its mature market.

Looking ahead, investors remain cautious. Despite strong earnings execution, Workday’s premium valuation, reflected in a P/E ratio of 126.43, requires consistent double-digit growth to justify its market cap of $60.7 billion. Without clear upside guidance, investors appear wary of near-term catalysts.