CFA Crunches the Numbers: Your Bitcoin Retirement Ticket to $100K/Year

Forget bonds and annuities—a chartered financial analyst just mapped the Bitcoin roadmap to six-figure retirement income. Here’s the cold, hard math.

The 21st Century Gold Rush

With traditional finance looking shakier than a meme stock’s fundamentals, the analyst reveals exactly how much BTC you’d need to generate $100K annually. Spoiler: It’s less than you’d pay for a Manhattan parking spot.

The Withdrawal Strategy Wall Street Hates

Using a conservative 4% annual drawdown rate (yes, even crypto retirees need guardrails), the target portfolio shakes out to—wait for it—2.5 BTC at current prices. Cue the institutional FOMO.

The Catch? Time Travel

This math assumes Bitcoin’s historical 200% annualized returns continue indefinitely. Because nothing says ’retirement planning’ like betting against the efficient market hypothesis.

One thing’s clear: The finance old guard isn’t just losing clients to crypto—they’re losing their monopoly on retirement math. Now if you’ll excuse us, we need to check if our ledger wallet counts as a 401(k).

GqENdF8WYAAyr4IGqENdF8WYAAyr4I

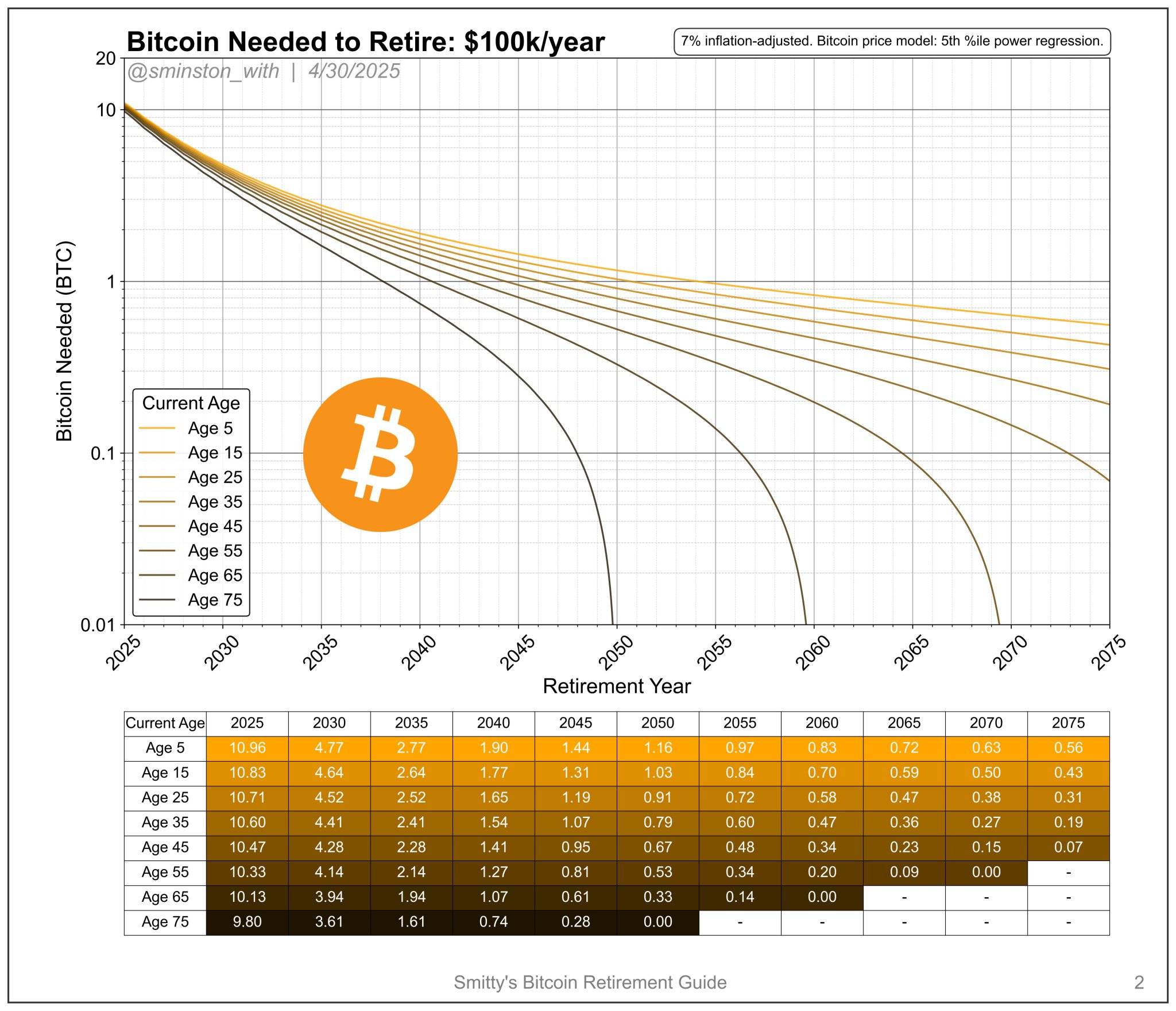

The model estimates how much BTC a person would need to secure a $100,000 annual income, adjusted for 7% inflation. Soni’s projections rely on a 5th percentile power regression model, meaning it reflects a low-end or worst-case growth path for Bitcoin’s price. This approach assumes gradual but steady BTC appreciation.

BTC Needs Vary by Retirement Timeline

According to the data, the number of Bitcoins needed to retire depends heavily on the year retirement begins. The earlier the retirement date, the more BTC is required. For someone currently aged 45 and planning to retire in 2030, the model estimates a need for 4.28 BTC.

At early 2025 prices, this equates to around $400,000. However, the BTC requirement drops over time due to the underlying assumption of Bitcoin’s future price growth.

If the same individual delays retirement to 2035, they would only need 2.23 BTC. By 2040, the number falls further to 1.41 BTC. For a 2045 retirement, only 0.95 BTC would be needed to support the same inflation-adjusted annual income.

Notably, the drop in the required amount in Bitcoin is due to the projection that Bitcoin’s price will continue to increase as the years progress. For instance, an investor who sought to retire five years ago with $400,000 would have needed 44.4 BTC in May 2020, as BTC traded at an average of $9,000 then. Now, this investor needs only 4.28 BTC.

Investor Behavior Show Disconnect with Projections

Despite these clear projections, many investors are hesitant to make the shift. According to Soni, a significant number of high-income individuals already have over $400,000 saved but avoid converting it into Bitcoin.

A key reason cited is reliance on financial advisers who may not understand or endorse Bitcoin. Soni notes that these advisers often discourage BTC investments, viewing them as speculative or risky. Strategy Chairman Michael Saylor recently suggested that by the time these advisors identify Bitcoin’s potential, the asset might have already reached $10 million.

GqENdF8WYAAyr4IGqENdF8WYAAyr4I

The model estimates how much BTC a person would need to secure a $100,000 annual income, adjusted for 7% inflation. Soni’s projections rely on a 5th percentile power regression model, meaning it reflects a low-end or worst-case growth path for Bitcoin’s price. This approach assumes gradual but steady BTC appreciation.

BTC Needs Vary by Retirement Timeline

According to the data, the number of Bitcoins needed to retire depends heavily on the year retirement begins. The earlier the retirement date, the more BTC is required. For someone currently aged 45 and planning to retire in 2030, the model estimates a need for 4.28 BTC.

At early 2025 prices, this equates to around $400,000. However, the BTC requirement drops over time due to the underlying assumption of Bitcoin’s future price growth.

If the same individual delays retirement to 2035, they would only need 2.23 BTC. By 2040, the number falls further to 1.41 BTC. For a 2045 retirement, only 0.95 BTC would be needed to support the same inflation-adjusted annual income.

Notably, the drop in the required amount in Bitcoin is due to the projection that Bitcoin’s price will continue to increase as the years progress. For instance, an investor who sought to retire five years ago with $400,000 would have needed 44.4 BTC in May 2020, as BTC traded at an average of $9,000 then. Now, this investor needs only 4.28 BTC.

Investor Behavior Show Disconnect with Projections

Despite these clear projections, many investors are hesitant to make the shift. According to Soni, a significant number of high-income individuals already have over $400,000 saved but avoid converting it into Bitcoin.

A key reason cited is reliance on financial advisers who may not understand or endorse Bitcoin. Soni notes that these advisers often discourage BTC investments, viewing them as speculative or risky. Strategy Chairman Michael Saylor recently suggested that by the time these advisors identify Bitcoin’s potential, the asset might have already reached $10 million.