Moody’s Axes US Credit Rating—Wall Street Braces for Debt Fallout

Another day, another downgrade. Moody’s just slashed the US credit rating—because apparently $34 trillion in national debt isn’t ‘AAA’ material anymore.

Wall Street’s sweating bullets as Treasury yields spike. Traders are scrambling to price in the new risk premium—while Congress keeps writing checks the economy can’t cash.

Funny how ‘full faith and credit’ doesn’t mean what it used to. Maybe they should’ve hodl’d those quantitative easing policies a little tighter.

Investors question Congress’ fiscal discipline

Carol Schleif, chief market strategist at BMO Private Wealth, warned that the downgrade might push investors to become more cautious. She said the bond market is watching “what transpires in Washington this year in particular.”

Schleif added that as Congress continues to negotiate, bondholders are ready to pressure lawmakers into sticking to stricter fiscal behavior. Moody’s became the last of the major ratings agencies to pull the plug. Fitch downgraded the US in 2023, and S&P made their MOVE all the way back in 2011.

Gennadiy Goldberg, head of US rates strategy at TD Securities, said the downgrade likely won’t force mass selling since most investment funds adjusted their rules years ago. But Goldberg also said the downgrade WOULD “refocus the market’s attention” on the tax-and-spending bill being debated in Congress.

Meanwhile, the Committee for a Responsible Federal Budget estimated that the bill could add around $3.3 trillion to the national debt by 2034. If temporary policies in the bill are extended, that number jumps to $5.2 trillion.

Moody’s also pointed out that multiple administrations have failed to reduce deficits and that it doesn’t expect current proposals to do much to change that.

Debt limit panic creeps into bond yields

Treasury Secretary Scott Bessent said the White House is trying to keep 10-year yields from spiking. The current yield is 4.44%, which is still lower than it was before TRUMP returned to office. But that number could change quickly.

Scott has also warned Congress that they need to raise the debt ceiling by mid-July. The US hit its borrowing limit back in January, and the Treasury has been using what it calls “extraordinary measures” to keep the government from defaulting. Without an increase, the country could run out of cash by August — the so-called X-date.

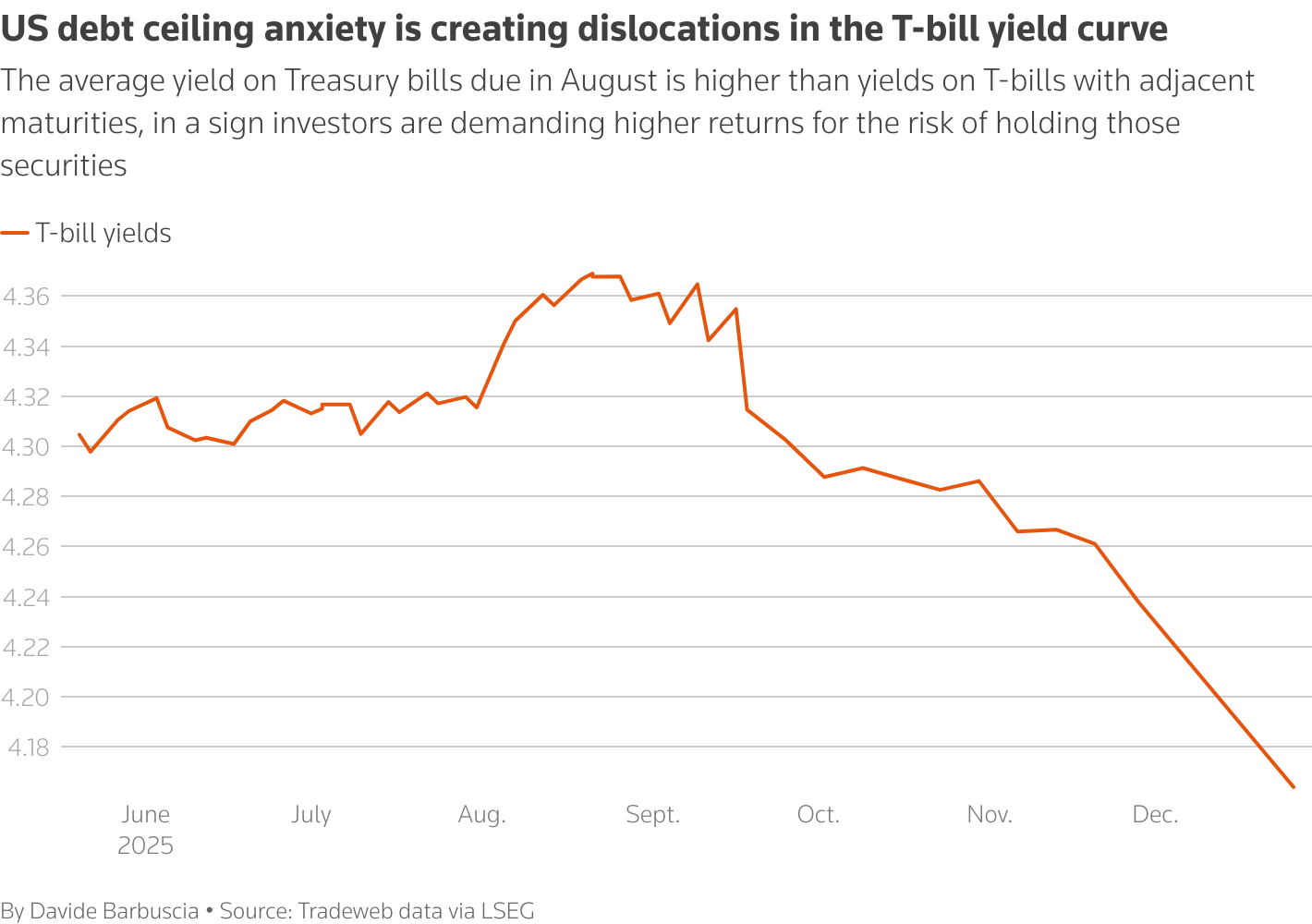

That fear is already showing up in bond prices. Yields on Treasury bills due in August are higher than those due before or after, signaling that investors are worried about a potential government cash crunch. Speaker Mike Johnson has said the House hopes to vote on the bill before Memorial Day on May 26.

White House rejects Moody’s downgrade as political

Harrison Fields, principal deputy press secretary at the White House, dismissed the downgrade and said the critics are “wrong, just as they were about the impact of Trump’s tariffs.” Fields claimed that the tariffs led to record investments, strong job growth, and no inflation.

Steven Cheung, communications director for the administration, went even further, calling Moody’s economist Mark Zandi a political enemy of Trump. Zandi works for Moody’s Analytics, a separate part of the company, and declined to comment.

Some analysts believe the final bill may not be as damaging as it seems. Barclays now projects that the deficit will grow by $2 trillion over the next ten years under the plan — a smaller number than the $3.8 trillion increase expected before Trump came back. They’re pointing to revenue from tariffs and other offsets as the reason.

But not everyone agrees. Michael Zezas, a strategist at Morgan Stanley, wrote in a recent note that the bill would increase the deficit in the NEAR term without giving the economy much of a boost.

Cryptopolitan Academy: Tired of market swings? Learn how DeFi can help you build steady passive income. Register Now

Log in to Reply

Log in to comment your thoughtsComments

Related Articles

|Square

Get the BTCC app to start your crypto journey

Get started today Scan to join our 100M+ users