Trump’s $8.7 Trillion Pension Gambit Could Be Crypto’s Next Big Break

Wall Street braces as Trump's pension overhaul threatens to unleash a tidal wave of capital into digital assets.

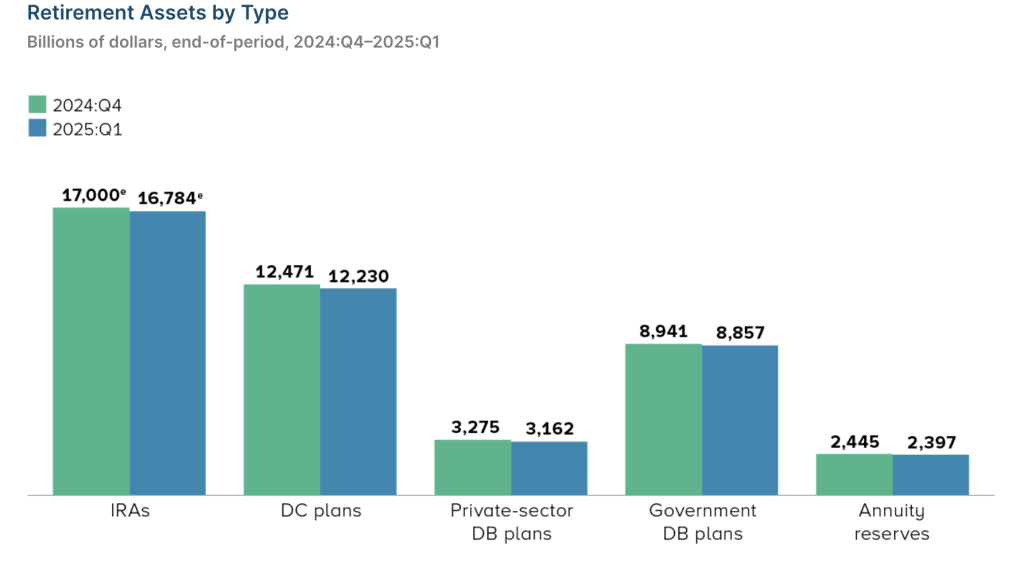

The $8.7 Trillion Shakeup

Washington's latest maneuver puts traditional retirement funds on notice—pension managers now face unprecedented pressure to diversify into alternative assets. Bitcoin and Ethereum stand as primary beneficiaries, with institutional adoption poised to skyrocket.

Crypto's Institutional Inflection Point

Wall Street veterans scramble to reposition portfolios while crypto exchanges report record institutional inquiries. The move bypasses decades of regulatory hesitation, forcing legacy finance to confront digital asset allocation head-on.

Washington Meets Blockchain

Political winds shift as policymakers acknowledge crypto's inevitable role in modern finance—though skeptics whisper about politicians finally understanding blockchain just in time to take credit for its rise.

Retirement accounts might finally escape the tyranny of 2% yields and overpriced fund managers. Because nothing says financial innovation like letting government pensions chase 100x crypto returns.

Why 401(k)s Are Different

The U.S. pension system rests on three pillars: Social Security, employer-sponsored plans like 401(k)s, and individual retirement accounts (IRAs). Among them, 401(k)s occupy a unique middle ground — widely used, automatically funded, and professionally managed, yet still shaped by individual choices from a preset menu.

According to the Investment Company Institute, 401(k)s account for nearly 30% of all individually directed retirement assets. Balances grow with age, averaging almost $300,000 for retirees over 65. This isn’t speculative capital — it’s middle America’s life savings.

Until now, those savings were limited to stocks, bonds, and mutual funds. Trump’s order gives them a new lever: exposure to digital assets.

Three Shifts Ahead

The impact of this MOVE is not just financial inflows. It could unleash three structural shifts — changing user behavior, institutional capital flows, and political dynamics.

1. Mainstream Breakthrough

Crypto’s toughest barrier has been trust among older, conservative investors. A 55-year-old worker opening a Vanguard 401(k) menu that lists a “Digital Assets Fund” alongside an S&P 500 index fund experiences a psychological shift. What was once viewed as a speculative gamble becomes a government-sanctioned, employer-endorsed retirement option.

That endorsement is powerful: it reframes crypto as part of mainstream financial life.

2. A Steady Capital Pipeline

ETFs opened the door for institutions, but flows remain sentiment-driven. 401(k) allocations work differently — they’re tied directly to payroll. Every payday, millions of dollars WOULD be funneled automatically into chosen funds, creating a stable and compounding stream of inflows.

This predictability will push asset managers like Fidelity and Vanguard to build diversified crypto products — baskets of Bitcoin, Ethereum, and perhaps blue-chip DeFi tokens, or hybrid portfolios mixing digital assets with stocks and bonds. The result: deeper liquidity and a more mature asset management ecosystem.

3. A Political Moat

Perhaps most importantly, the policy could insulate crypto from partisan swings. U.S. administrations have long oscillated between openness and hostility toward digital assets, discouraging long-term capital. By linking crypto to retirement savings, the calculus changes: any future government restricting crypto would risk being seen as “cutting into my pension.”

That binding of financial interest to political survival may force both parties toward greater policy consistency — cementing crypto within America’s long-term financial agenda.

Optimism With Caveats

The upside is clear. Even if just 5% of 401(k) assets shifted into crypto, that’s roughly $400 billion — an order of magnitude larger than recent ETF inflows. Combined with regulatory clarity and mainstream acceptance, it could catalyze a revaluation of the entire asset class.

But challenges remain:

- Adoption: More than 60% of 401(k) assets sit in traditional mutual funds. Convincing savers to shift toward volatile assets will take time.

- Risk: Retirement money is sensitive to market swings. Regulators and managers must define guardrails and disclosure rules to protect participants.

- Design: Will offerings focus narrowly on Bitcoin and Ethereum, or extend to a broader universe? How much volatility will plans allow, and how will funds smooth it?

The answers will decide whether this becomes a watershed moment — or a policy experiment that stalls under its own weight.

The Starting Gun

Trump’s order is less a conclusion than a beginning. By tying the future of crypto to America’s most conservative capital — pensions — it accelerates the sector’s shift from speculative fringe to structural pillar of finance.

The seas ahead are vast: trillions in potential inflows, new product classes, and political realignment. They are also uncertain: adoption hurdles, regulatory detail, and volatility risk remain.

But the symbolism is already clear. When retirement accounts begin to treat crypto as a serious asset class, the door to a new financial era is no longer hypothetical. It’s swinging open.

Disclaimer: The opinions in this article are the writer’s own and do not necessarily represent the views of Cryptonews.com. This article is meant to provide a broad perspective on its topic and should not be taken as professional advice.