Bitcoin Champion Demands Federal Reserve Include BTC in Stress Tests—Here’s Why It Matters

Pressure mounts on the Fed to recognize digital gold in its financial health checks.

The New Frontier of Financial Resilience

A prominent voice in the cryptocurrency space is pushing the U.S. Federal Reserve to update its rulebook. The call? To formally add Bitcoin to the battery of stress tests it administers to the nation's largest banks. This isn't just a request—it's a challenge to the traditional framework of what constitutes a reserve asset.

Stress Tests Meet Digital Assets

These regulatory drills simulate economic nightmares—deep recessions, market crashes, soaring unemployment—to see if banks can survive the storm. Advocates argue that ignoring Bitcoin creates a blind spot. As institutional adoption grows, treating BTC as a theoretical non-factor is a gamble. It’s like testing a ship's integrity while pretending the rising tide of digital finance doesn't exist.

Why The Fed Might Hesitate

Regulators cling to models built for a pre-blockchain world. Volatility remains the classic rebuttal, the go-to reason for keeping crypto at arm's length in formal risk assessments. Yet, this stance increasingly looks like guarding a fortress while the financial landscape evolves into something entirely new outside its walls.

The Bottom Line for Finance

Incorporating Bitcoin into stress tests would signal a seismic shift. It would move BTC from the fringe of 'alternative investment' toward the core of institutional balance sheet considerations. Of course, to some in traditional finance, this sounds as sensible as asking a submarine to stress-test for a meteor strike—a classic case of preparing for yesterday's crisis with yesterday's tools.

The push is on. Whether the Fed listens will reveal more about its view of the future than any spreadsheet ever could.

Extreme Volatility Demands Separate Treatment

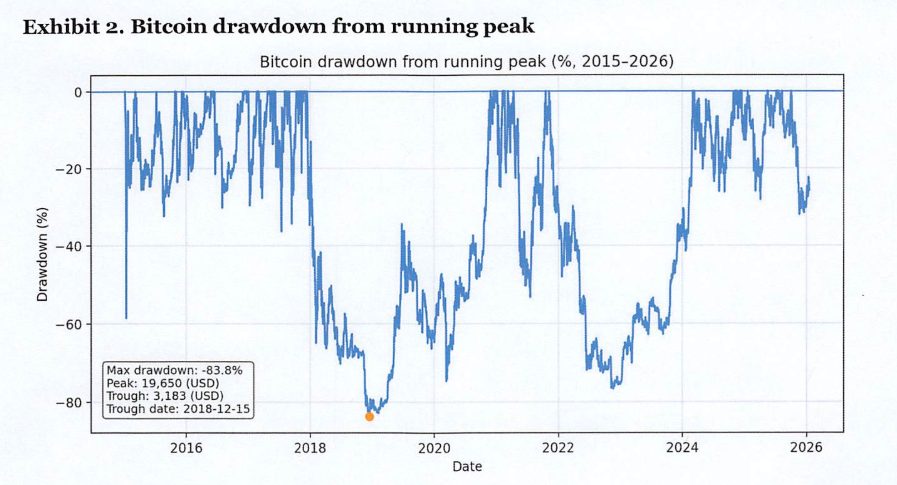

Rochard’s letter presents a detailed analysis showing Bitcoin’s 73.3% annualized realized volatility over the 2015-2026 sample period, compared to just 18.1% for the S&P 500 over the same timeframe.

The analysis documents a maximum drawdown of 83.8% from peak to trough, with daily return tails ranging from -10.0% at the 1st percentile to 10.7% at the 99th percentile, far exceeding typical asset behavior.

“Bitcoin’s risk profile is unusually idiosyncratic and materially non-linear: it has experienced repeated, deep peak-to-trough drawdowns and sustained periods of very high realized volatility,” Rochard wrote.

He argued these properties affect valuations, margin requirements, counterparty exposures, and liquidity demands “in ways that cannot be reliably inferred from other scenario variables.“

The submission includes rolling correlation analysis demonstrating Bitcoin’s unstable dependence structure with macro-financial variables, with correlation between Bitcoin and S&P 500 returns ranging from negative to strongly positive across 90-observation windows.

Rochard warned that “a fixed ‘beta’ mapping from equities (or risk sentiment) to bitcoin will understate risk in some regimes and overstate it in others,” making explicit scenario variables essential for consistent stress testing across banks.

Implementation Would Reduce Model Divergence

Rochard recommends that the Federal Reserve provide quarterly bitcoin price paths for baseline, adverse, and severely adverse scenarios, with optional daily paths for global-market-shock datasets.

He suggests three calibration methods:

- Historical feature matching tied to peak-to-trough drawdowns and realized-volatility percentiles

- Regime-switching time-series models with different volatilities for bull and bear markets

- Jump-diffusion frameworks with stochastic volatility explicitly representing tail risk

“The calibration goal is not to forecast bitcoin, but to supply a consistent and severe, but plausible, path that stress tests can translate into market and counterparty outcomes,” Rochard explained.

He emphasized that firms without Bitcoin exposure could simply ignore the variable, while those with direct or indirect exposure WOULD gain “transparency, reproducibility, and consistent scenario translation” rather than relying on inconsistent proxy assumptions.

The timing coincides with broader market stress, as Bitcoin plunged to $88,000 amid $1.07 billion in liquidations over 24 hours while gold surged past $4,800 per ounce.

The divergence has renewed debate over Bitcoin’s role as either a risk asset or a strategic reserve, particularly after President Trump’s threats to impose tariffs on Greenland triggered a flight from US assets.

CEO of Galaxy, Mike Novogratz, noted “the gold price is telling us we are losing reserve currency status at an accelerating rate,” adding that Bitcoin “is disappointing as it is still being met with selling.”

The gold price is telling us we are losing reserve currency status at an accelerating rate. The long bond selling off is not a good sign either. $BTC is disappointing as it is still being met with selling. I will reiterate it has to take out 100-103k to regain its upward…

— Mike Novogratz (@novogratz) January 20, 2026The Federal Reserve’s comment period for the 2026 stress test scenarios closes February 21.

Senator Cynthia Lummis, who previously criticized potential government Bitcoin sales as squandering “strategic assets while other nations are accumulating bitcoin,” has proposed legislation to acquire up to 1 million Bitcoin over five years through budget-neutral methods, including tariff revenue and revalued gold reserves.