French Borrowers Face Credit Crunch as Lending Stagnation Sparks Alarm

France's credit pipeline is seizing up—and borrowers are left holding the bag.

The Squeeze Is On

Banks are slamming the brakes on loans, turning the screws on everyone from first-time homebuyers to small businesses. No official numbers yet, but the whispers in Parisian boardrooms suggest Q2 approvals dropped harder than a baguette off a bicycle.

Why This Hurts

With inflation still gnawing at purchasing power, frozen credit lines force families to choose between overpriced rentals and praying for a lottery win. Meanwhile, fintechs are circling like vultures—offering "innovative" solutions at 20% APY, naturally.

The Silver Lining?

DeFi platforms see an opening. Ethereum-based lending protocols just hit record EUR deposits as savers flee traditional banks. Because nothing says "financial stability" like trusting an anonymous smart contract with your life savings.

France's financial guardians promise intervention. But after last year's 'temporary' capital controls? We'll believe it when we see it—preferably in writing, notarized, and triple-checked by a blockchain oracle.

In Brief

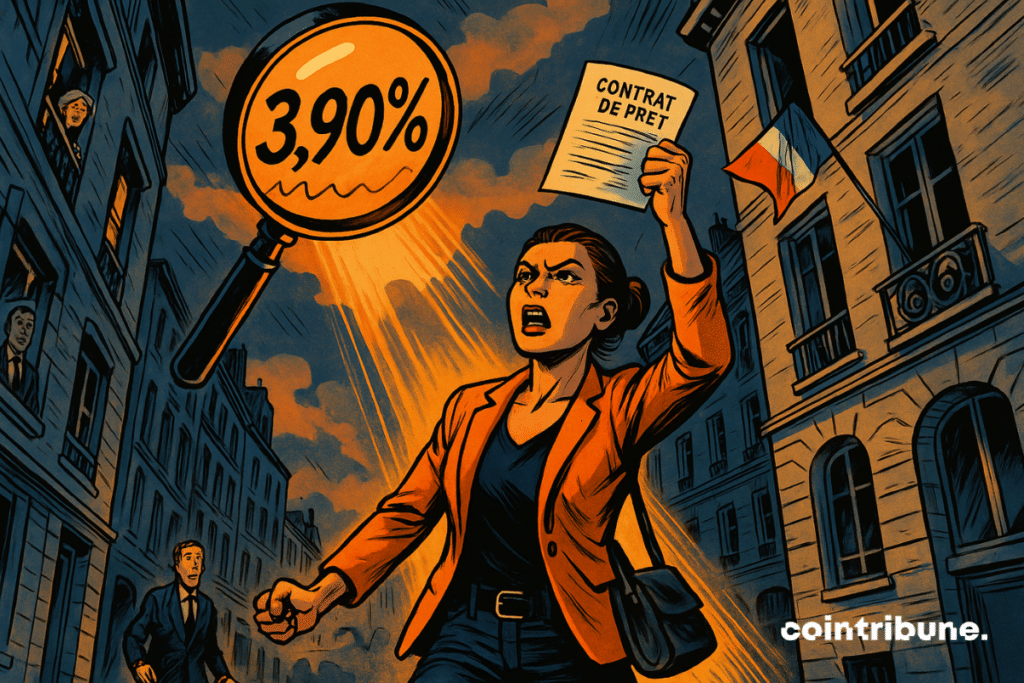

- Mortgage rates have stopped falling for three months, despite a recovery in sales of older properties.

- After exceeding 4.5 % at the end of 2023, rates dropped to around 3 % in spring 2025, then froze.

- This stagnation is explained by banks’ prudence, preferring to preserve margins amid economic uncertainty.

- This new reality forces buyers and investors to rethink their medium- and long-term financing strategies.

Rates Freeze Despite Market Recovery

While loans are surging again in France, interest rates on loans have stagnated for three months. This stability contrasts with the downward trend that began at the end of 2023, when rates reached peaks above 4.5 % for loans of 20 years or more.

Driven by this gradual easing, the real estate market has regained some vigor. Transaction volumes in older properties rose by 8 % in the first half of 2025. The BPCE Observatory even estimates that the year could end with 959,000 sales, of which 85 % WOULD concern older properties. However, although fundamentals appeared aligned to prolong the downward move, the rates have now frozen.

The current stagnation is explained by a combination of economic and behavioral factors. Data from banking barometers clearly show that the downward movement has stopped, leaving a plateau :

- Rates for 20-year loans have now stabilized around 3 %, after a sharp drop from their peak at the end of 2023 ;

- Real estate prices have remained generally stable, limiting leverage effects for borrowers ;

- Banks, despite a more dynamic market, have not adjusted their rate scales for several months, favoring a controlled profitability approach ;

- Borrowing conditions have considerably eased, but without triggering further rate decreases since spring.

In short, while borrowers benefit from more favorable conditions than in 2023, the rate decline seems to have reached a technical floor, at least in the short term.

Towards a Structural Normalization of Banking Conditions

The current calm is not a temporary coincidence but the result of a deeper shift in banking policies. Major brokers like Vousfinancer and Cafpi have noticed a stabilization of rate scales since spring 2024, which continues into 2025.

“Rates remain unchanged in most banks,” Vousfinancer states in its monthly report published at the beginning of July. Average levels now sit around 3.20% for 20-year loans, or even 3.35% depending on the profiles. This apparent calm hides a more selective lending logic.

Banks remain commercially aggressive but are more focused on files they consider strategic. Julie Bachet, General Manager of Vousfinancer, explained : “Banks remain in customer acquisition mode while increasingly targeting profiles that interest them.”

This results in occasional but limited offers: reduced rates for first-time buyers, subsidized loans for homes with good energy performance ratings (DPE) or energy renovation projects. CIC, Crédit Mutuel, LCL, and Banque Populaire offer specific products at conditions below market rates, but these initiatives remain targeted and conditional. Outside these privileged profiles, standard rates no longer change.

This new balance appears durable. The Governor of the Bank of France, François Villeroy de Galhau, recalled on France 2 in early June: “We will not see again the exceptionally low rates around 1.5 % that we had four years ago.”

In this credit blockage and instability of borrowing conditions environment, some investors are turning to alternatives uncorrelated to classical bank rates. Bitcoin, in particular, is gaining visibility as a SAFE haven asset and diversification tool.

Its decentralization, independence from monetary policies, and direct accessibility attract a growing segment of savers, frustrated by the slowness of traditional financing. This renewed interest highlights a shift in wealth strategies, at a time when traditional credit levers struggle to reactivate.

The prospect of a return to floor rates is thus definitively fading, despite a recovery in the real estate market. For borrowers, this means that current conditions, ranging between 3 % and 3.5 %, could become the norm. While this stabilization may reassure in the short term, it also demands a revision of long-term strategies, for both individuals and investors.

Maximize your Cointribune experience with our "Read to Earn" program! For every article you read, earn points and access exclusive rewards. Sign up now and start earning benefits.