Why We Need More Stablecoins: The Unstoppable Rise of Digital Dollar Alternatives

Stablecoins aren't just surviving—they're fundamentally reshaping global finance while traditional banks scramble to keep up.

The Digital Lifeline for Modern Finance

These crypto-anchored assets provide what volatile cryptocurrencies can't: predictable value. They bridge the gap between traditional finance's stability and crypto's borderless efficiency—without the heart-stopping 20% daily swings.

Bypassing Banking Bottlenecks

Stablecoins slash settlement times from days to seconds. They ignore banking hours, bypass intermediary fees, and operate where traditional banking infrastructure simply doesn't exist. Nearly 1.7 billion adults remain unbanked worldwide—stablecoins represent their fastest path to financial inclusion.

The Institutional Tipping Point

Major payment processors and corporate treasuries now integrate stablecoins into their operational DNA. They're not speculating—they're optimizing. While traditional finance debates regulation, stablecoins already move billions daily with fewer hiccups than some national banking systems.

Let's be real: if banks could innovate at crypto's pace, we wouldn't need stablecoins. But watching legacy institutions try to digitize money is like watching a giraffe on ice skates—technically possible, but painfully awkward for everyone involved.

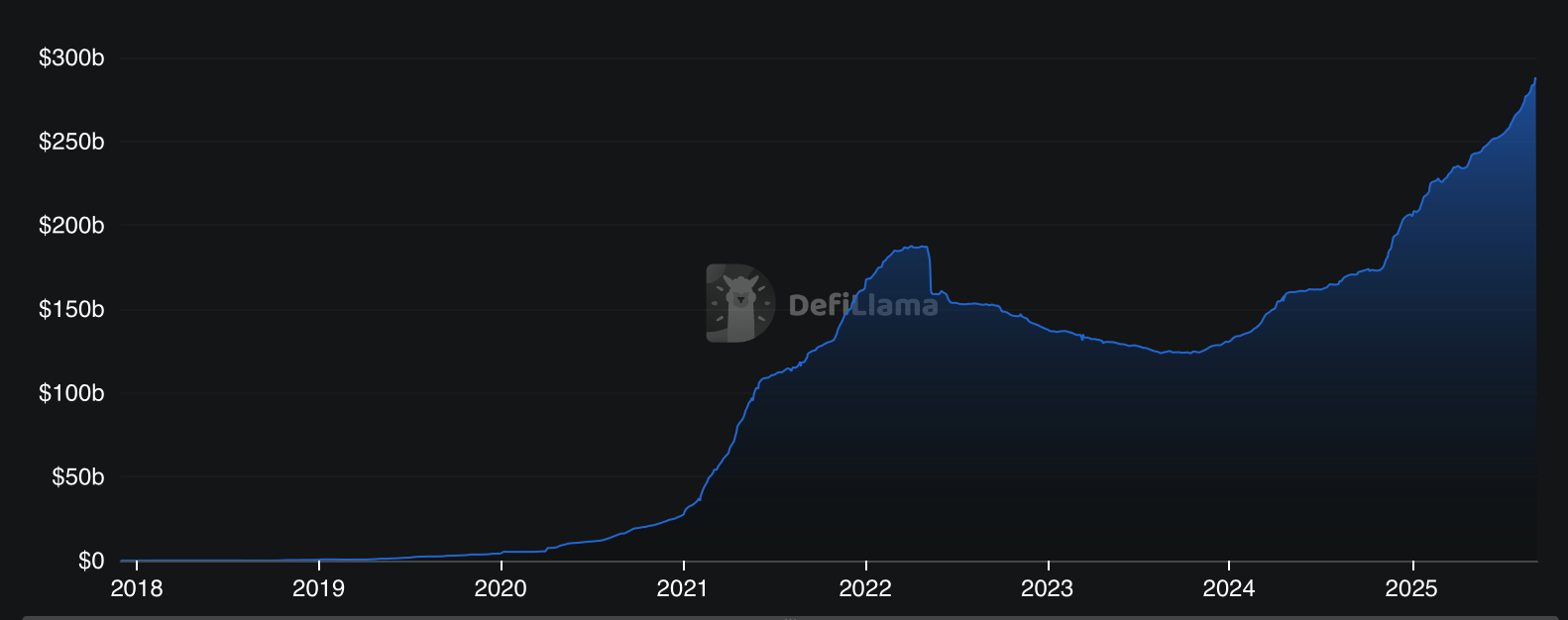

Total market cap of stablecoins is over $280 billion Source: Defillama

We’re seeing a rush of companies launching stablecoins in the U.S. because issuers finally gained clarity with the passing of the GENIUS Act in July 2025. For the first time, the U.S. government clearly defined who can issue stablecoins, what counts as a “payment stablecoin,” and what obligations issuers have to consumers.

Since the GENIUS Act passed, MetaMask rolled out mUSD, Stripe launched a payments-focused chain called Tempo, Circle announced their purpose-built stablecoin payments L1, Arc Network, and there’s been a spree of acquisitions. Stablecoin infrastructure companies like Iron are getting snapped up, and traditional finance firms like Stripe are spending heavily to buy crypto companies (Privy and Bridge) whose products they can fold into their existing offerings.

In addition, chains are launching their own stablecoins as a way to capture more revenue from the yield they generate. MegaETH has its native stablecoin, USDm. Hyperliquid launched USDH, which sparked a bidding war with Paxos, Agora, Sky, and Frax all vying to get involved.

At this rate, it’s easy to imagine a world where every serious company in crypto eventually issues its own stablecoin. Which raises the obvious question: do we need more?

: Even as the number of unbanked people falls, over 1.3 billion remain without access to banking, mostly in places with unstable currencies. Stablecoins provide 24/7 access to money online, without borders. If companies like PayPal push stablecoins directly to existing customers, they could onboard more people to use the global money rails of crypto.

: In the real world, we don’t have one currency. We have dollars, euros, yen. The same should be true onchain. If everything settles in dollars, the entire crypto economy becomes dependent on U.S. monetary policy. More stablecoins means less over-reliance on a single standard.

: Right now stablecoin markets are concentrated into the hands of a few big players. With more stablecoins, concentration risk decreases. If one issuer faces technical, regulatory, or solvency issues, users WOULD have alternatives to pivot to without destabilizing the broader ecosystem. More issuers mean more redundancy, making the system safer.

Stablecoins are quietly rewriting the rules of global finance. They give anyone, anywhere, access to money that moves instantly, across borders, with incentives aligned to users rather than banks. The more competition, the better. If crypto transforms the global economy, it won’t be because of speculation. It will be because of stablecoins.