Pump.fun Is Raking In Fees – But Does $PUMP Actually Capture That Value? Data-Driven Showdown Versus $GOOD’s Real Revenue Share Model from goodcryptoX

Fee machines are humming—but who actually collects the profits?

Pump.fun's revenue engine hits new peaks daily, yet token holders question whether $PUMP truly benefits from the platform's explosive growth. Meanwhile, goodcryptoX’s $GOOD token implements a transparent revenue-sharing mechanism that directly distributes earnings back to stakeholders.

The Revenue Reality Check

Not all tokenomics are created equal. While some projects promise value accumulation, others deliver tangible returns. $GOOD’s model allocates a fixed percentage of platform fees directly to token holders—no loopholes, no vague promises.

Transparency Versus Hype

In a space flooded with speculative assets, real revenue share stands out. It’s the difference between hoping for reflection and actually receiving dividends. GoodcryptoX built a system that rewards holders consistently, not conditionally.

A Tale of Two Tokens

One thrives on transaction volume, the other on sustainable distribution. As Pump.fun’s fee generation soars, the critical question remains: does the value trickle down, or does it just pool at the top? Meanwhile, $GOOD’s structure ensures that as the platform grows, so do stakeholder payouts—no creative accounting required.

Because in crypto, if you’re not getting a share of the fees, you’re probably paying them.

The crypto landscape has evolved significantly after the lessons of “DeFi Summer” in 2020, where many projects relied on inflationary token emissions, resulting in over 1.8 million tokens dying in 2023 alone. It taught a brutal lesson: sky-high APYs funded by printing tokens out of thin air inevitably lead to a death spiral. Investors learned the hard way with the collapse of Terra/Luna and Celsius that if a project isn’t a real business, it’s a ticking time bomb. As a result, the market has shifted towards valuing sustainable models.

This evolution has spotlighted a paradigm known as “Real Yield.” As detailed in in-depth research by CoinLaunch, projects gaining long-term traction are often those that generate real revenue and share it with token holders. This means income derived from business activities, such as Pump.fun’s fees from token launches, rather than token emissions. This principle is also discussed by experts at Zeebu and the CFA Institute as a move beyond pure speculation.

Pump.fun, the launchpad at the center of the pump fun solana ecosystem, is a powerful revenue generator. As of August 14, 2025, the platform has generated over $724 million in cumulative revenue. On the surface, this makes its token, $PUMP, appear attractive. However, applying the professional analytical framework by CoinLaunch raises an important question: how efficiently does the platform’s success translate into value for individual $PUMP token holders?

This analysis will examine the Pump.fun model, explore its value accrual mechanisms, and contrast it with goodcryptoX ($GOOD) — a project with a different economic design.

An Analytical Toolkit: A 6-Point Framework for Evaluating Token Models

To assess a project’s sustainability, we can use a framework similar to that of a venture capitalist. The CoinLaunch framework provides six key areas for analysis:

Let’s apply this framework to the pump fun token.

Deconstructing the $PUMP Token: An Analysis of Value Accrual

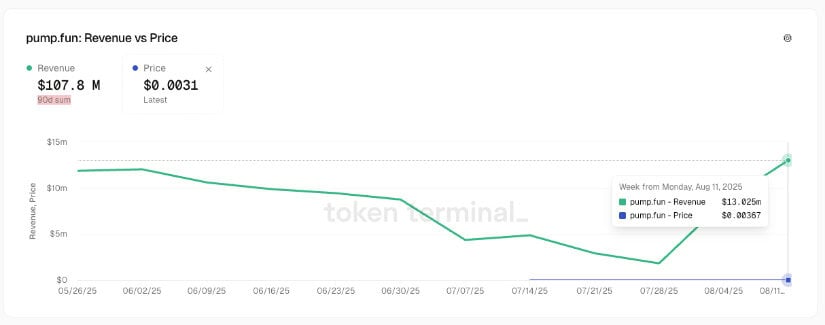

While Pump.fun’s revenue is substantial, its token model utilizes an indirect approach to value distribution. The platform’s success in the pump fun crypto space is undeniable, but as on-chain data from Dune Analytics shows, its operational success and token holder value are two distinct topics.

Source: TokenTerminal

-

Value Accrual & Sharing Mechanism: An Indirect Approach. A key feature of the model is that platform revenue does not flow directly to $PUMP holders as a dividend or yield. Instead, the model relies on token buybacks. While the team deposited millions in SOL to Kraken for buybacks, the token experienced an 11.85% post-listing drop, illustrating that such mechanisms can be influenced by broader market forces. Though revenue remains high, as tracked by DefiLlama, our analysis suggests this model is less direct in delivering value to holders compared to a pure revenue-sharing model.

-

Token Growth Potential: A High Initial Valuation. The unofficial Pump.fun coin launched with an alleged FDV of over $6.6 billion, a figure available on platforms like CoinGecko. From an analytical standpoint, a high initial valuation can present a challenge for significant future price appreciation. It is a mathematical near-impossibility for it to achieve a 10x (current level of USDC) or even a 5x growth (current level of TRON and Lido) from this level without real utilities.

Source: CoinGeko

-

Ecosystem Exposure: Concentrated on a Single Narrative. The platform’s business model is primarily focused on the meme coin narrative on the Solana blockchain. This concentration presents a long-term risk. As seen in this Dune comparison dashboard, the 80% drop in Pump.fun volume and revenue in July, corresponding with a cooling of meme coin hype and competition from platforms like LetsBonk.fun, highlights this sensitivity.

Source: DuneAnalytics

-

Revenue Distribution: A Wide Holder Base. The large number of token holders means that the impact of mechanisms like buybacks is distributed across a very wide base. Any potential future implementation of a direct revenue share would similarly be divided among a large number of participants.

goodcryptoX ($GOOD): A Utility-Driven Alternative with Direct Revenue Share

Now, let’s analyze goodcryptoX ($GOOD), a project with a different design philosophy.

goodcryptoX is an established trading platform with 400,000 users and over $5 billion in processed volume, primarily via its CEX-focused app. The project’s key innovation is bringing its suite of CEX-grade algorithmic Trading Bots to the DEX world, including strategies like DCA, Grid, and Trailing Algos across five major chains.

This utility-driven approach resulted in a 9.3x growth in DEX volume from March to July, with further catalysts like perpetuals trading on the roadmap.

Let’s analyze the $GOOD token through the same framework:

- Value Accrual & Sharing Mechanism: A Direct Model. The model is straightforward: 50% of all DEX trading revenue is shared directly with $GOOD holders. Additionally, 10% of platform revenue is used for buybacks and burns, creating both a direct “real” yield and a deflationary mechanism.

- Token Growth Potential: A Lower Initial Valuation. $GOOD is launching with an initial market cap of ~$531k and an FDV of $25 million, according to its profile on CoinLaunch. This presents a different starting point compared to a large-cap asset like $PUMP – a realistic potential for exponential growth.

- Revenue Distribution: A Concentrated Initial Holder Base. With only 4.33% of the total supply allocated to the presale, the initial revenue stream will be shared among a smaller group of ~400 holders, which includes strategic VCs like Fenbushi Capital and Cointelegraph.

- Yield & Holder Risks: Illustrative Yield and Market Dependence. Based on historical volume data, the annualized yield (APY) for token holders would have been ~ 100%. This figure is illustrative and not a guarantee of future returns, as yield depends entirely on ongoing platform activity. There is no mandatory lock-up period for earning this yield. However, the model’s success is dependent on the team’s execution and its ability to grow trading volume in a competitive market.

Comparative Analysis: Two Different Token Models

| Brand Recognition | Very High, Dominant Market Position | Growing, Established User Base |

| Value Accrual Mechanism | Indirect (Team Buybacks) | Direct (50% Rev-Share) + Buy & Burn |

| Token Growth Upside (FDV) | ~$6.6B+ (Limited Upside) | ~$25M (High Growth Potential) |

| Ecosystem Exposure | Concentrated (Dependent on Solana Meme Coins) | Diversified (Multi-chain, low direct competition, diverse product)

) |

| Demand on Revenue | High (Widely Distributed) | Low (Initially Concentrated) |

| Current Yield | None (Speculative Price Action) | ~100% APY (Based on Historical Data) |

Two Philosophies of Value

Pump.fun is a highly successful product that has demonstrated strong revenue generation. Its token model is designed around indirect value accrual through buybacks, aligning holder success with the platform’s overall market perception and growth.

In contrast, goodcryptoX and its $GOOD token offer a different philosophy — one based on direct participation in the platform’s cash flows. This model is built on tangible utility, a diversified product offering, and a commitment to sharing a significant portion of its revenue directly with token holders.

The choice between these models depends on a participant’s individual strategy and what they look for in a token. One represents exposure to a dominant brand’s market performance, while the other offers a stake in the revenue of a growing utility-focused business. As the market matures, both models will likely find their place, but for those specifically seeking direct, sustainable yield, the differences are clear.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. All figures are illustrative and based on historical data, which is not indicative of future results. Please conduct your own thorough research and consult with a professional financial advisor before making any decisions.