Vitalik’s Delusion: Why Ethereum Can’t Become the Next Google

The Ethereum dream hits reality's wall—and the cracks are showing.

Blockchain's golden child faces scaling nightmares that make Google's early server problems look like child's play. Gas fees that rival Wall Street brokerage commissions, transaction speeds that crawl when they should sprint, and a developer exodus that's becoming harder to ignore.

The Infrastructure Illusion

Ethereum backers tout its decentralized web vision, but building on this foundation feels like constructing a skyscraper on quicksand. Network upgrades promise paradise while delivering purgatory—developers face constant postponements and compromised functionality.

The Corporate Cold Shoulder

Major enterprises that should be flocking to Web3's promise instead maintain cautious distance. They see the technical debt accumulating faster than ETH staking rewards. When Fortune 500 companies choose private chains over Ethereum's mainnet, the message echoes louder than any blockchain conference keynote.

Finance's Final Jab

Wall Street watches with amused detachment—another 'disruptive' technology struggling to scale beyond cryptocurrency speculation and NFT jpegs. The real disruption seems to be Ethereum's ability to disrupt its own roadmap every eighteen months.

Vitalik's vision once inspired a generation. Now it risks becoming blockchain's most beautiful—and most expensive—pipe dream.

Low-risk DeFi – A New Growth Engine for Ethereum?

As BeInCrypto reported, Vitalik Buterin suggested that low-risk DeFi protocols like Aave or MakerDAO could become a primary revenue source for ethereum (ETH). He likened this model to how Google derives much of its revenue from Google Search.

“Importantly, low-risk defi is often very synergistic with a lot of the more experimental applications that we in Ethereum are excited about.” Vitalik observed.

Applied to Ethereum’s case, Vitalik emphasizes that the network needs SAFE financial activities that support savings and payments—especially for underserved communities—to preserve the ecosystem’s cultural identity.

This view from Vitalik has sparked lively debate. David Hoffman states that low-risk DeFi does not generate much blockspace demand for Ethereum. Nevertheless, locking large amounts of ETH in lending protocols like MakerDAO, Aave, or Uniswap elevates ETH into a form of “commodity money” within the Ethereum ecosystem.

Some developers argue that low-risk DeFi is universal, simple, and scalable to billions of users. Stani Kulechov has envisioned a day when AAVE could distribute yield to billions globally, turning DeFi into a foundational financial tool for humanity.

“Low-risk DeFi is Ethereum’s workhorse: simple, powerful, and universally useful. One day, Aave could be distributing yield to billions across the globe.” Stani commented.

Low Revenue, Hard to Justify the Valuation

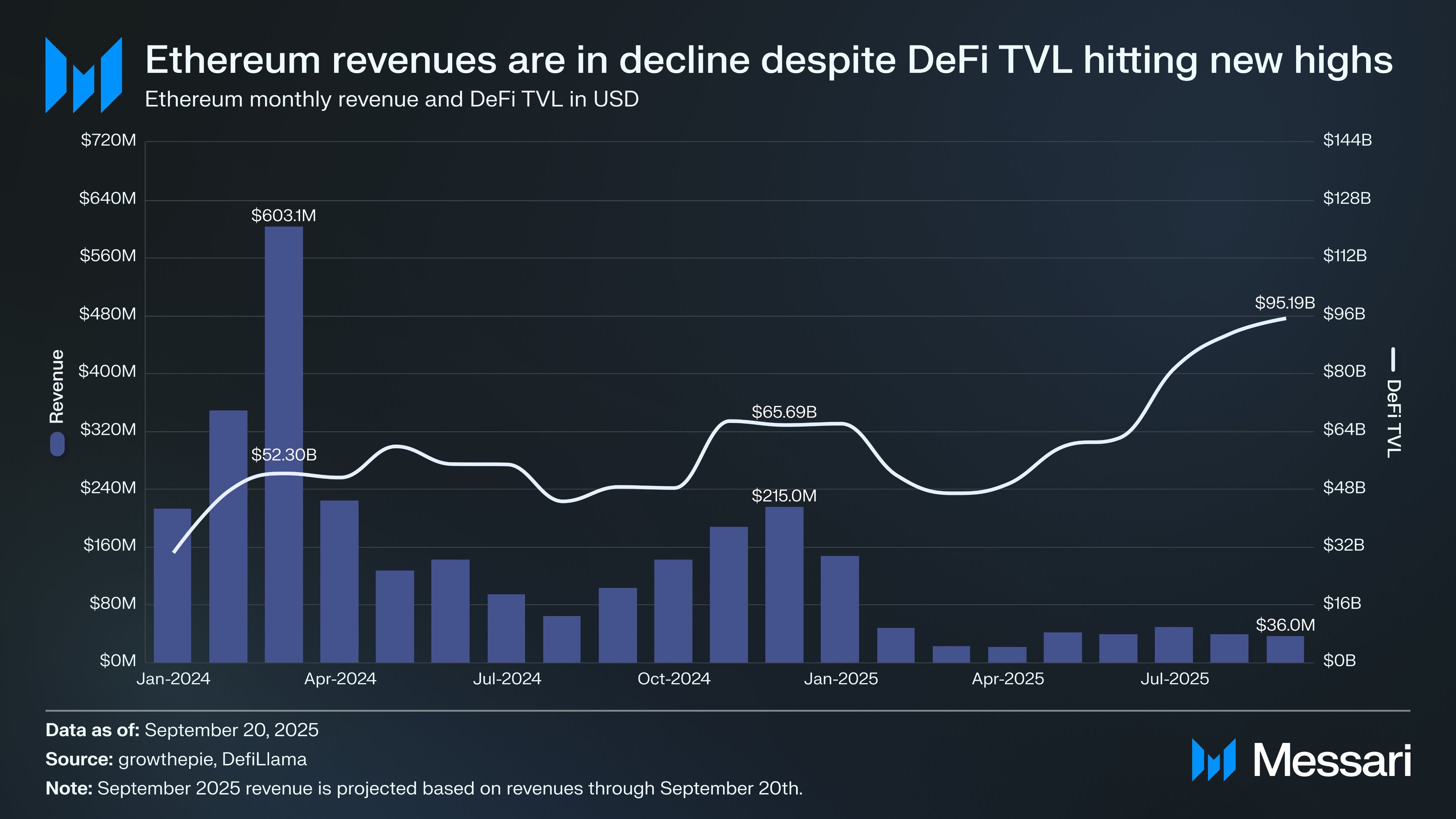

Not everyone agrees with Vitalik. Another X user argues that low-risk DeFi alone cannot justify Ethereum’s enormous market cap, currently about $0.5 trillion. Trading volume from these protocols reached only around $36 million in September—a figure far too small to create sustained cash FLOW for the network. Moreover, despite DeFi’s TVL of roughly $95.2 billion and a stablecoin supply of $161.3 billion, these metrics still do not generate enough blockspace demand to keep network fees attractive for validators.

“Low-risk DeFi as Ethereum’s ‘Google Search’ can only work if it prioritizes ETH as the primary monetary asset. However, with stablecoins dominant and many pushing Ethereum as the ‘RWA chain,’ ETH must compete with an ever-increasing field of monetary assets for this position,” a user on X shared.

Another commentator warns that Vitalik’s framing of serving the unbanked via low-risk DeFi misstates the practical objective. They caution that moving lending/borrowing markets entirely on-chain at Layer-1 degrades user experience and reduces composability. Ethereum also struggles to compete with dedicated payment systems like Stripe or Circle, or fee-optimized chains like Solana, where high MEV subsidizes low costs.

Competition with Stablecoins and RWAs

Another strand of thought holds that Ethereum is in fierce competition with stablecoins and RWAs to retain the role of the ecosystem’s native monetary asset. While RWAs may attract users with yield, they are unlikely to match ETH’s reliability and liquidity; thus, ETH retains an edge as an unmatched monetary asset.

Notably, some analysts stress the appeal of neutral chains like Ethereum as a custody LAYER for centralized assets such as USDC or RWAs. Holding USDC on Aave via Ethereum may be less susceptible to intervention by Circle than storing it on centralized enterprise chains, increasing Ethereum’s attractiveness as a censorship-resistant infrastructure.

Although some see the idea of “nationalizing” Core DeFi protocols on Ethereum as the right direction, many experts believe Ethereum is not yet ready to provide low-risk, low-cost, highly scalable DeFi services. This remains an endgame target that goes beyond merely on-chain lending/borrowing.

“Enshrined services is the real endgame (one step beyond what Vitalik is saying here), but it should not be limited to lending.” an expert shared on X.